Whether you’re just starting a family or nearing retirement, the end of life can seem far away and difficult to imagine. While there’s no need to dwell on it, preparing now can help you and your family feel more secure in the years to come.

“End-of-life planning” is a broad term that includes making financial, healthcare, and other decisions about what happens before, during, and after death. Those decisions can help you make sure your wishes are carried out when the time comes and provide financially for your family after you’re gone.

You’re probably familiar with life insurance, wills, and trusts, but are you wondering how they’re different? Not sure if you should leave everything to a named beneficiary vs. your estate? Unclear which planning documents you really need?

Life insurance and wills are both important parts of end-of-life planning for many people. They work in different ways to support your family after your death. In some cases, a trust can help provide more detailed instructions to make sure your wishes are carried out.

Here’s a closer look at how they might fit into your own retirement planning. (As always, consult an attorney if you have questions about wills or trusts.)

What is life insurance?

Life insurance is a form of insurance that provides a cash payout upon your death. If you die while the policy is active, your insurance company will distribute a lump sum of money, called a death benefit, to the person you’ve named on your life insurance policy. This person is called a beneficiary and might be a spouse, an adult child, your grandchildren, or another close relative. It’s possible to name more than one beneficiary, and you can also name an organization or charity as a beneficiary.

The goal of life insurance is to provide financial protection to the people that matter to you after death. The money comes with no strings attached, so your family can use it for many purposes, like paying funeral expenses, covering bills, paying your mortgage, and saving for college. If you have people depending on you financially, life insurance helps make sure they’re not burdened financially after your death, especially if it’s unexpected.

What is a will?

A will is a legal document that lays out your final wishes and leaves instructions on how to distribute your property after you die. Your will can cover things like whom you want to receive your personal items and money, how to pay any remaining expenses, and who should care for your minor children.

When you die, your will specifies how your assets should be distributed to the people or organizations you’ve named in it. Collectively, these assets are known as your “estate.” To create a will, you’ll need to choose an executor, who is responsible for making sure the will is carried out. Your executor is different from your heirs, who are the people or organizations that you name to receive your assets.

Your will directs something called probate, which is the legal process for distributing your assets. During probate, any assets you didn’t promise to certain people, like the wedding china you want to go to your daughter, are divided among the heirs listed in your will.

There are some exceptions to what you can include in your will, though. A will can’t cover assets you own with other people, like a house, or assets with a beneficiary, like life insurance.

Can I use my will to distribute life insurance death benefits?

Generally, no. When you die, your life insurance payout goes to the person or people named on the policy. You can’t use your will to change the beneficiary named in your life insurance policy.

One of the main purposes of your will is to provide instructions for distributing your assets, from your home to your jewelry. Assets include anything of value that you own, which is why your life insurance death benefit doesn’t count during the probate process. Since your life insurance payout is meant for your life insurance beneficiary once you die and only payable after your death in most cases, it’s not typically considered an asset and not included in a will.

There is one exception, though. If all of your beneficiaries die before you, then your life insurance will be paid to your estate vs. a beneficiary. If this happens, the terms of your will dictate how the life insurance proceeds are distributed. If you don’t have a will, your life insurance is distributed based on the laws in your state.

Putting your life insurance in a trust

Wondering how trusts fit into the end-of-life planning picture? A trust is another estate planning tool that can be helpful in special situations.

A trust is an account where you can put certain assets and provide instructions for who can access them and when. It’s managed by a trustee whom you name when you create the trust. Your trustee can be the same person or a different person from the executor of your will. These documents are both part of your estate plan.

You can name a trust vs. another beneficiary, like a partner or child, to receive the payout from your life insurance policy. You can also indicate in your will that your assets should go into the trust instead of being distributed directly to your loved ones.

Why would you want to do that? Since you get to decide on the trust instructions, you have more control over when your beneficiaries can access the death benefit and how they spend the payout. For example:

- You can give your family a steady stream of income. With life insurance, your death benefit gets paid out all at once. This can be difficult for some families to manage, especially with term or permanent policies that can top $2 million. By putting your life insurance policy in a trust, you can have that death benefit paid out in annual installments over time, so your family has a more predictable stream of income to rely on.

- You can reserve the money for specific purposes. Life insurance money comes with no strings attached, so your beneficiaries can use it for whatever they feel is best. But what if you have specific wishes for where that money goes? Putting it in a trust lets you set rules about the use of the funds. For example, you might want it to go toward your children’s education or buying a family home.

- You can leave behind money for young children. Naming your minor children as beneficiaries on a life insurance policy is a no-no, since they’re not legally allowed to receive the money. If you’re a single parent and want to make sure your policy goes to your young kids, one way to accomplish that is with a trust. Create a trust that will pay out the benefit to them once they’re legal adults, or name a trustee who can use the money while they’re still children to cover their day-to-day needs.

Creating a trust is a little more complex than a will and involves extra costs to maintain. For some people, those complexities are worth it to gain more control over how family members use their life insurance money or other assets. If you think a trust is the right decision for you and your family, consider talking to an attorney to make sure it’s set up correctly.

Does life insurance go through probate?

No. Since life insurance is paid directly to your beneficiaries, it doesn’t go through your will or through the probate process. That’s why it’s such a valuable way to leave behind funds for loved ones to use after your death.

A few of the main benefits of life insurance living outside of your will include:

It’s Faster Than Probate.

It can take months for your will to be read, in many cases. During that time, there are still bills to pay and mortgage payments to make. Those costs can put a strain on your family while they’re waiting for the estate to be settled. One in four people say they would feel the financial effects within a month if the primary wage earner in their household died, according to the 2020 LIMRA study. In contrast, life insurance claims are typically paid out quickly once your beneficiaries submit a claim, giving your family the support they need during a tough time.

The Benefit Isn’t Subject to Estate Taxes or Debts.

During probate, the court looks at all your debts before distributing your assets. If you owe money on a car loan or student loans, for example, your estate might have to pay them off before your assets are distributed. For example, if you have $100,000 in a savings account and a $20,000 car loan that needs to be paid, then only $80,000 of that savings account will be left for your heirs.

Instead of putting off a life insurance purchase because of debt, consider how a policy can help protect your family from debt later. If you’re paying off significant debts, life insurance is a way to leave money behind that won’t be reduced by any debts you owe.

The payout from a life insurance policy also isn’t subject to taxes in most cases, since you pay your premiums with after-tax dollars. That means your family will get the full payout they’re counting on to cover expenses and save for the future. For example, if you have a $100,000 term life policy and die while it’s active, your family will receive the full $100,000 as a lump sum cash payment. That $20,000 credit card debt won’t affect it, and your family isn’t required to use that money to pay credit cards or other debts.

You Choose Where the Money Goes.

Are you concerned that a family member will try to take control of where your money goes after your death? You’ve probably heard horror stories about family members feuding over assets. During probate, it’s possible for someone to step in and contest the will, which means more time, money, and complexity to sort it out. It also means your money might not end up going where you intended.

Creating a will and keeping it up to date is one way to avoid this, but life insurance can also help.

So does a will supersede a life insurance beneficiary? Or can an executor override a beneficiary? Your family or the executor of your will can’t override your choice of where the death benefit goes. If it’s important to you that your second spouse receives the money or you want to make sure to leave a nest egg for a grandchild, life insurance can give you confidence that those wishes will be carried out.

Should you have both a will and a life insurance policy?

A will and a life insurance policy are both important to prepare for the end of life, even when it’s hopefully decades away. They work together to help your family pay for expenses after your death.

They’re also planning steps that many people often put off. According to a 2021 LIMRA study, nearly half (48%) of American adults don’t own any life insurance, up 2 percentage points from 2020. The number of people without a will is even higher: 67% of adults don’t have one as of 2021, up 9 percentage points from 2017.

If you haven’t taken these steps yourself, it’s not too late. Life insurance and wills are both investments that you have to put in place before you need them, so now’s the time.

How to create a will

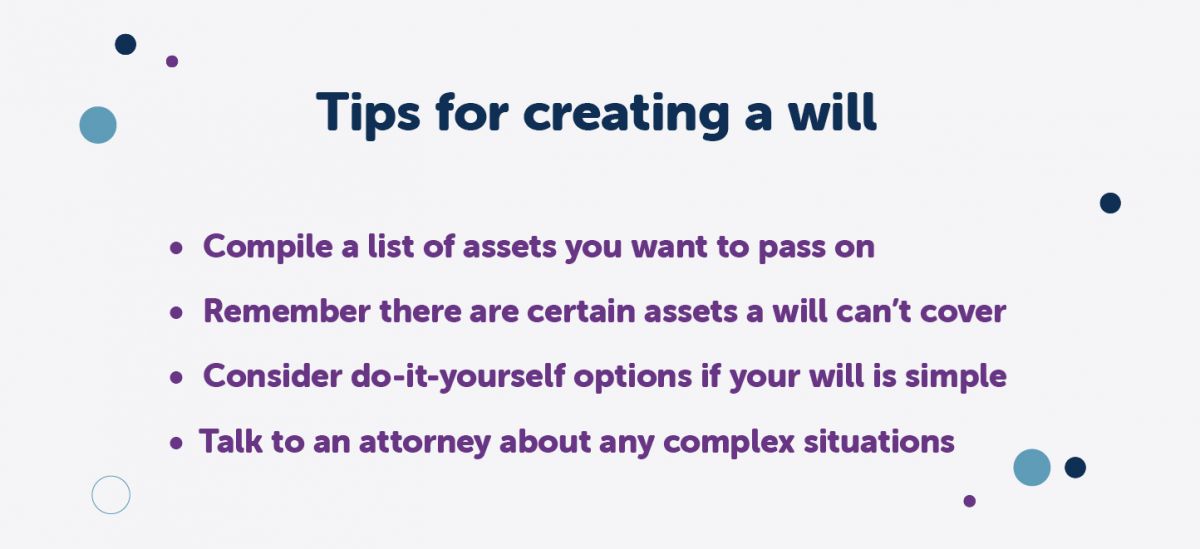

To prepare a will, begin by compiling a list of your assets and debts. Be sure to include the contents of safe deposit boxes, family heirlooms, and other assets that you wish to transfer to a particular person or entity. If you want to leave certain personal property to specific heirs, you should start a list of those items to include in your will. Keep in mind that there are certain assets a will can’t cover, like a home you own with someone else, life insurance policies, and other investment accounts with a beneficiary.

There are several ways to go about creating a will, including the do it yourself (DIY) route and going to an attorney. Making a will yourself is simple and cost-effective, and there are plenty of options to take care of it online. If you have any complex considerations, like second marriages or children with disabilities, it’s often worth it to work with an attorney to make sure that everything is executed properly.

One caution: Once your family discovers your will isn’t sufficient, it’s too late to make sure it’s done correctly. Even if you choose to do it yourself, you might want to have a professional review it.

How to buy life insurance

When shopping for life insurance, you’ll first need to decide how much life insurance you need. The right amount is different for everyone based on budget, financial goals, and other factors. To come up with your figure, add up all of your assets and expenses over the period of time you want to protect your family. You should also consider your future expenses and goals, existing life insurance coverage you might have, and any outstanding debt. Our life insurance calculator can help you find the right amount.

You’ll also need to decide what kind of life insurance to buy. If you’re still in the prime of life, term life insurance is the simplest and most cost-effective way to protect your family’s future. Term life insurance offers coverage for a specific period of time, usually 10 to 30 years, to help replace your income, pay the mortgage or other debts, or make sure your partner has enough saved for retirement.

As you get older, final expense insurance can help you plan for funeral expenses or other costs that come up at the end of life. Designed for adults over 50, final expense insurance provides a way for your family to pay for a funeral, burial or cremation, medical bills, and other expenses, without having to wait months for your estate to be settled in probate. Coverage amounts are lower than a traditional term life or permanent life policy, which helps keep payments affordable. Approval is also typically quick and simple.

Once you’re ready to buy, you can purchase a life insurance policy over the phone or online with Fidelity Life. You’ll also need to name your beneficiary when you buy the policy.

Updating your will and life insurance

Your will and life insurance policy are both documents you may have for years, or even decades. A lot can change during that time, from marriages and babies to divorces and deaths. It’s important to keep both documents updated so that your assets go where you want them to go. There are a few tips to keep in mind:

- You can choose different beneficiaries for your will and your life insurance policy. There’s no rule that says they have to be the same. If you choose multiple people, you can assign different amounts in both cases. For example, you might want 80% of your life insurance payout to go to your spouse and 10% to go to each of your two children so your spouse has enough immediate funds to live on. In your will, you might want your assets to be equally split among the three. Your will also allows you to be more specific about who you want to receive meaningful belongings or family heirlooms like your grandmother’s jewelry or your father’s antique clock collection.

- Updating your will is not the same as updating your life insurance. You need to keep both your will and your life insurance updated to avoid unintended consequences. One doesn’t govern the other. For example, if your spouse is the sole beneficiary on your life insurance and dies before you, the life insurance payout would go to your estate and get distributed during probate, where it could be reduced by debts. Some states also charge probate fees that can eat into your payout even more.

- Review both regularly, including after major life events. Updating your life insurance beneficiary is usually as simple as filling out a form. To update your will, make sure to reflect your choices clearly in writing and bring in your original attorney if needed. Give these documents a scan regularly to make sure the beneficiaries are living and reflect your current choices. It’s typically good to do this once a year or after any big life milestones, including weddings, deaths, and births.

- Make sure your beneficiaries know your wishes. Choosing the right beneficiaries is the first step. The next is making sure they’re aware of your wishes. With a will, the most important person to inform is your executor. Since they’re in charge of carrying out everything outlined in the will, it should be someone you trust to carry out your wishes. It can also be helpful to let your heirs, or the people that you’ve chosen to receive your belongings, know that you’ve named them to avoid confusion or disagreements when the time comes. With life insurance, you should inform your chosen beneficiary or beneficiaries. If you’ve chosen secondary beneficiaries, or people to receive the money if your primary beneficiaries die, you might want to let them know about the backup plan as well. You should also make sure your beneficiaries know where to find the paperwork and how to carry out their duties when the time comes. Keep your life insurance policy, will, and any trust documents in a safe spot.

Still have questions about life insurance beneficiary vs. will?

We’re here to help you learn more about life insurance. If you have questions, reach out to our agents at (855) 291-6365.

At Fidelity Life, our goal is to make life insurance simple, affordable, and understandable for everyday families. This content is intended for educational purposes only. Each post is carefully fact-checked, reviewed, and updated regularly to ensure the information is as relevant as possible.