Annuity vs. life insurance

Protecting your family’s future is an important part of any financial plan. That said, there are plenty of ways to go about it.

Life insurance policies and annuities can both provide a financial cushion for you and your family later on when you need it. There are some key differences to keep in mind, though. Here’s what you need to know about an annuity vs. life insurance.

How does life insurance work?

Life insurance provides financial support to your loved ones after your death. When you buy a life insurance policy, you enter into a contract with your life insurance company. You make regular payments, called premiums, to keep your policy active.

In exchange, the insurance company agrees to provide a cash payout if you pass away while the policy is in place. That money comes with no strings attached, so your loved ones can use those funds for anything they need: to pay bills, replace your paycheck, or cover a child’s college tuition.

Life insurance comes in two main types: term and permanent life. The main difference? How long your policy lasts. Term life covers you for a set period of time and is more affordable than permanent coverage. Permanent plans, on the other hand, last your entire life as long as you keep making payments. This type of coverage can also build cash value over time, which you may be able to tap into while you’re alive.

Ultimately, life insurance is a financial investment in your family. The payout from a policy doesn’t benefit you, it benefits the people who matter most to you. If your family is depending on you financially, life insurance can provide the security they need, even during a tough time.

How do annuities work?

An annuity is another type of insurance that provides a guaranteed income stream while you’re living. You agree to pay the insurer, either in a lump sum or through a series of payments. In exchange, the insurer promises to pay a series of cash deposits over your lifetime to bolster your income.

Annuity payouts are typically structured like an installment plan, where you receive regular payments over time. These payments can begin within a year of buying the annuity or decades later, depending on the contract. Annuities come in several varieties, including fixed, equity indexed, and variable products.

Annuities can provide extra income to people who are concerned that they don’t have enough saved for retirement, or who want to invest in their family’s future ahead of time. Some people choose annuities as an alternative to savings accounts or other investments.

Similar to other retirement products, annuities are often subject to different taxes and fees. Some costs to look out for include upfront commission fees and high surrender fees or penalties for withdrawing funds early.

What is the difference between an annuity and life insurance?

With either life insurance or an annuity, you pay money in exchange for a financial benefit. The major difference between annuity and life insurance policies? They offer different types of protection.

Annuities provide an income stream during your lifetime so that you won’t outlive your assets. You receive the benefits from the plan, and the money is intended to help cover your own expenses in your later years. Since payments can begin as quickly as within a year after purchasing the annuity, some people use annuities to supplement retirement income from Social Security payments, a pension, or a 401(k). Life insurance, on the other hand, is designed to protect loved ones financially after you die. Your family receives the payout, not you, helping them meet immediate financial needs and reach longer-term goals.

Another key difference: The amount you invest in your plan upfront. Some annuities require a lump sum payment that could reach into the hundreds of thousands of dollars. With life insurance, on the other hand, you make regular payments into your policy. Those payments are typically monthly, although you may be able to make them annually or on another schedule. For some people, smaller regular payments can make it easier to fit an investment like life insurance into the family budget.

Types of life insurance

When considering a life insurance or annuity investment, do a little research first on the products available to you. Your options for life insurance include:

- Term life insurance: Term life insurance provides a guaranteed death benefit for a specific period of time, generally between 10 and 30 years. Easy to understand and affordable, term life is a good fit for most families. Term life plans offer affordable, flexible coverage during times when you have big financial responsibilities, like while you’re paying off your mortgage or raising a family. If you die unexpectedly, your family can use the payout to replace your income and cover expenses.

- Permanent life insurance: A permanent life insurance policy remains in place for the rest of your life as long as you make your premium payments. These types of plans also come with a cash value feature, which acts as an extra income source during your lifetime. The policy builds value over time, so you can borrow from your policy to cover expenses while you’re still living. One common form of permanent coverage is whole life insurance, which has level payments and a cash payout that won’t change over time. If you’re considering whole life insurance vs annuity products, you’ll see they have one key thing in common: they build cash value over time. With a permanent policy, you can typically access the accumulated cash value after a few years. Keep in mind that you’ll need to pay back any money borrowed from your cash value for your beneficiary to receive the full death benefit later.

- Final expense life insurance: A final expense life insurance policy is a type of permanent coverage with a lower death benefit. Designed for people between 50 and 85 years old, final expense can help pay for funeral costs or other end-of-life expenses after your death. Since the cash payout is smaller, it’s typically easy to qualify for a policy.

Types of annuities

Annuities also come in several varieties, depending on when you’d like them to pay out and how you’d like to earn income from them.

When choosing a payment schedule, you have two main options:

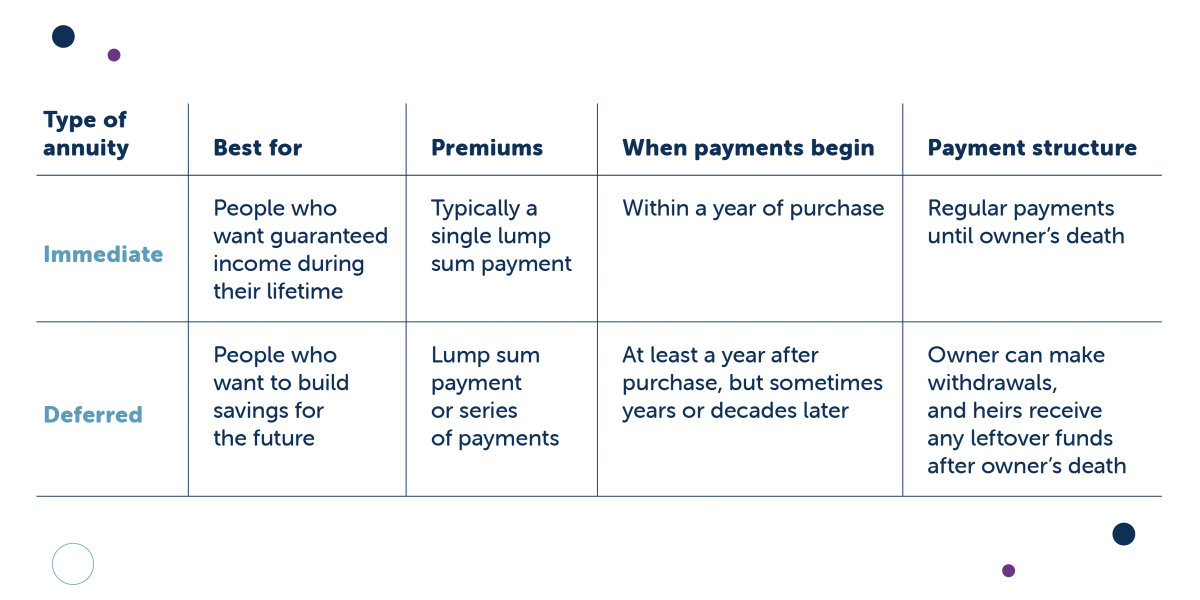

- Immediate annuities are designed for people who want quick returns from their annuity. You’ll typically make a one-time payment, and the annuitization phase (when your annuity pays out) begins within a year of that payment and continues until your death.

- Deferred annuities are designed for people who want to put away money now for their later years. During the accumulation phase, you pay a lump sum or make a series of deposits into an account. The annuitization phase begins a minimum of one year after you open the account, but can be years or even decades later.

With both immediate and deferred annuities, you can choose the type of return you’ll receive from your investment. Your main options are:

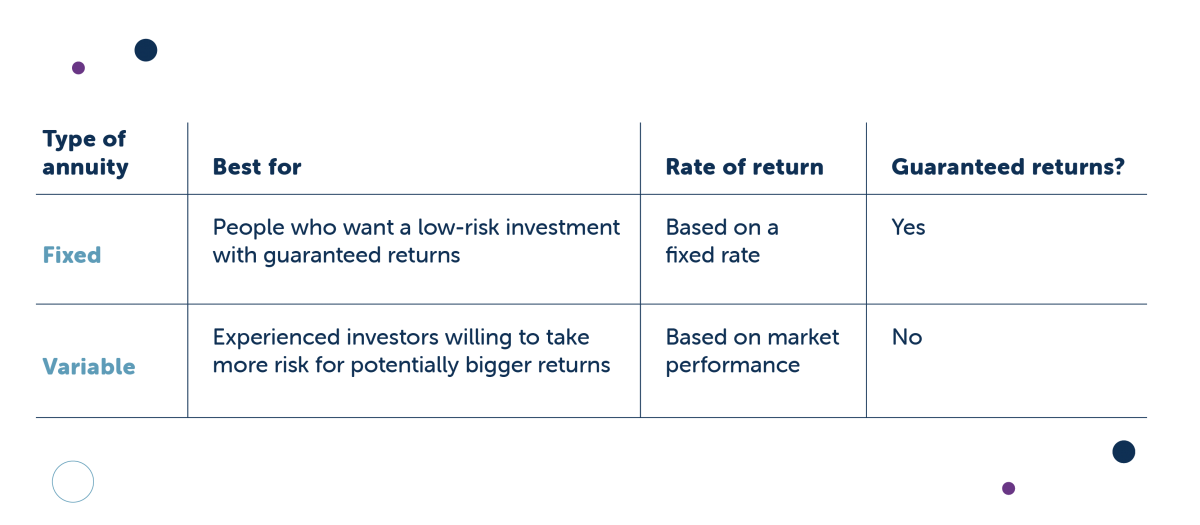

- Fixed annuities, which earn a fixed interest rate while you’re accumulating money in the annuity. You can either make a single payment or a series of payments, and your money will grow based on that interest rate. When the annuitization phase begins, you’ll receive fixed payments based on a set dollar amount, interest rate, or preset formula.

- Variable annuities, which are similar to mutual funds and can fluctuate based on market performance. Your insurance provider invests the money you put into the annuity, and your payouts from the annuity depend on how the investments perform. Variable annuities can potentially deliver higher returns than fixed annuities, but also have the risk of losing value if they don’t perform as intended.

Choosing term life insurance vs. an annuity

Trying to decide between term life insurance vs annuity? Think whole life insurance might be the way to go? The right choice depends on what you need your insurance to do, both now and in the future.

Here are a few things to consider before you decide:

Who Needs the Money.

Annuities are generally intended to cover your own expenses while you’re still living and fill retirement income gaps with their cash value. Annuity benefits can often be left to a beneficiary after the annuity owner dies. In this case, the insurance company typically distributes any remaining payments to the beneficiary as a lump sum or stream of payments. Life insurance benefits are paid after your death, and you can choose how your family receives those payments. If the goal is to protect your family financially after you’re gone without digging too far into your current assets, life insurance is typically the better bet.

Tax Considerations.

Tax issues may be a factor in choosing an annuity vs. a life insurance policy. Earnings from annuities may be considered taxable income, so you’ll still be responsible for paying taxes on some portion of the payments. A life insurance payout is generally tax-free, on the other hand, so your family won’t need to pay taxes on the payout once they receive it. Consult your tax or financial advisor before purchasing any annuity.

Your Age.

It’s typically best to buy life insurance while you’re young, so you can lock in the best rates. In contrast, people often consider annuities when they are older or planning for retirement.

Still have questions?

We’re here to help. Get in touch to talk with one of our agents about your life insurance options or start your online life insurance quote today.

At Fidelity Life, our goal is to make life insurance simple, affordable, and understandable for everyday families. This content is intended for educational purposes only. Each post is carefully fact-checked, reviewed, and updated regularly to ensure the information is as relevant as possible.