Term life insurance is designed to protect you and your family exactly when you need it, for as long as you need it. These plans provide coverage for a set period of time, whether you’re filling a gap before retirement or need coverage until your house is paid off and your kids are out of school.

Term life plans are generally more affordable than permanent life insurance, which covers you your whole life and allows you to build cash value. This makes term life a good bet for most families. But how do you figure out how long you’ll need coverage? Here’s what you need to know about choosing a term life plan length.

What is a term length?

A “term length” indicates how long your policy lasts. Most term life plans run from 10 to 30 years. You can choose whether you want short-term or longer-term coverage, depending on your unique financial needs.

If you die while your term life insurance policy is active, your family receives a lump sum of cash they can use to cover day-to-day expenses and replace your income. It can also help to pay off any debt, bills, or end-of-life expenses that you’ve left behind.

Once you reach the end of your term, you have a few options. You may be able to renew your policy and extend the coverage period, apply for a new policy altogether, or just let it expire if you don’t need coverage anymore.

How do I calculate my term length?

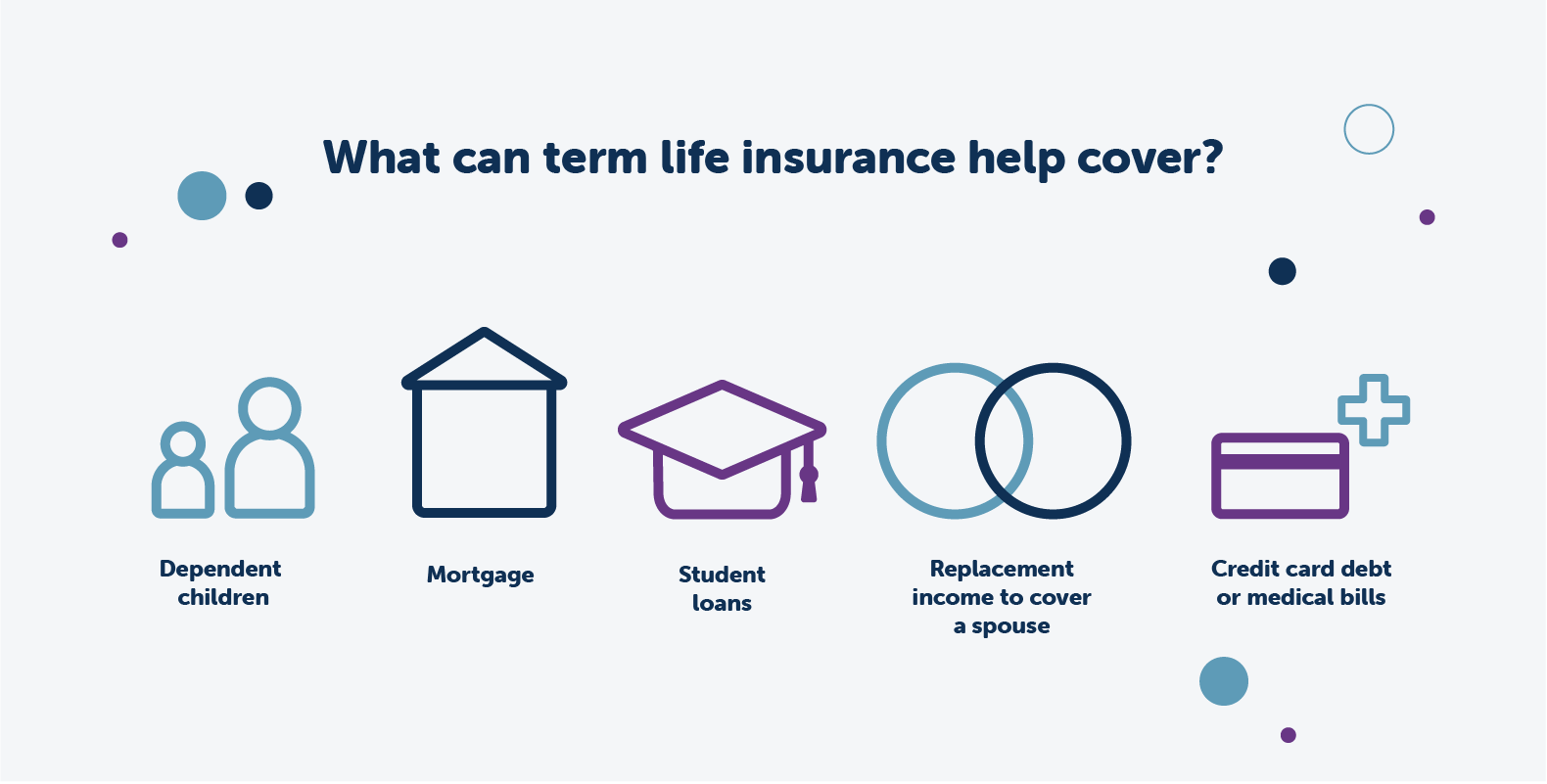

Finding the best term length for you starts with factoring in all your expenses and responsibilities. Since you’re buying life insurance to protect your family financially, consider how long you’ll need that protection to cover any current and future needs like:

- Dependent children

- Mortgage

- Student loans

- Replacement income to cover a spouse

- Credit card debt or medical bills

Depending on your stage of life, your ideal term length can vary. If you are getting married, starting out in a new career, or planning to have kids, you might want a 30-year term to cover you and your family through these major life changes. Most mortgages last for 30 years, so a 30-year term life can also be a good fit if you’ve just bought a house.

If your kids are in college and you only have a few years left on that mortgage, a 10- or 15-year plan might work better. Also, make sure to round up your term length if needed. Paying off your mortgage in 13 years? Get a 15-year term for maximum protection.

A few other things that can impact term length include:

- Consider how much life insurance you can afford. On average, longer term lengths tend to cost more than shorter term lengths. That said, life insurance is much more affordable than most people think, so you may be able to afford more than you realize.

- Your eligibility for certain term lengths can partially depend on age and health. For example, some insurers won’t approve you for a 30-year term plan after a certain age, so talk to an insurance agent about your options.

Why it pays to consider a longer-term length

If you’re weighing your options, here’s why you might want to consider a longer policy:

- It will never be cheaper than it is now. Your life insurance rates go up each year, so now is the best time to get a good deal on a longer-term policy. If there’s a chance you’ll need it later, consider buying ahead of time so that you’re covered no matter what.

- To protect against the unexpected. Life happens – new babies, layoffs, new houses, and medical emergencies can all impact your financial obligations. You may have the math worked out now, but things can change.

- In case you’re not able to qualify later. Health issues down the road may make it more expensive and harder for you to qualify for coverage. It’s better to lock in coverage now for as long as you may need it, so you can have peace of mind for the future.

At Fidelity Life, we’re committed to helping you find the right term length and coverage to fit your financial needs so you can protect your family. For more information, give us a call or start your online quote today.

At Fidelity Life, our goal is to make life insurance simple, affordable, and understandable for everyday families. This content is intended for educational purposes only. Each post is carefully fact-checked, reviewed, and updated regularly to ensure the information is as relevant as possible.