Term Policy Life Insurance

Term life insurance offers flexible and affordable coverage for as long as you need. But how long is that, exactly? Here’s how to pick the right term length for you and your family.

What is term policy life insurance?

Term life is a life insurance policy purchased for a specific length of time. If you buy a life insurance policy and die during the term, your life insurance company pays a lump sum of cash called a death benefit to the beneficiary of your policy. Term life is the most affordable and flexible type of life insurance, making it a good fit for many families.

What does life insurance term length mean?

When you buy term life insurance, you’ll choose a set number of years for your coverage to last. That number of years is the “term” of the policy. Common term lengths include 10, 15, 20, and 30 years.

Consider the length of time your family may benefit from having life insurance when choosing a term life policy. Do you want to cover just a short length of time in the next decade or so, while you’re finishing up paying a mortgage or until your kids are out of the house? Do you want your family to have coverage for a longer period to create a bigger safety net? Choose your term life insurance length based on those specific goals.

How long should you get term life insurance for?

When it comes to selecting a term policy, life insurance coverage should provide you with peace of mind for as long as you need it. There’s no magic answer to how long you should get term life insurance for, since it depends on why you’re buying it. The best choice for you and your family will depend on your unique situation, financial obligations, and future plans.

Anyone buying life insurance should start by identifying current and future expenses, like living costs, groceries, mortgage, or car payments, and saving for college or retirement, as well as current assets like savings or investments. This helps identify the gap between your resources and expenses, so you can pick a coverage amount that works for you.

Certain factors can make some term lengths a better fit for you or affect your term options. Here are a few things to consider:

Your Age

The younger you are when you purchase life insurance, the more options you’ll have. For example, it’s often easier to qualify for a 30-year policy in your 20s or 30s than in your 50s.

Life insurance costs also go up as you get older, so you can save on a policy with a longer life insurance term length by purchasing sooner. Consider how long you need protection vs. the term length options available to you. If you’re still in your 20s and planning on starting a family, it may pay off long-term to lock in that 30-year policy now to protect your family for the long haul.

Your Health

Just like your age, life insurance is more affordable the healthier you are. People in good or great health can typically secure longer term lengths at more competitive prices than people with health issues. In some cases, a complicated medical history may make it harder to qualify for certain types of plans or term lengths.

Your Dependents

Protecting loved ones is the main reason life insurance exists. Ultimately, it’s not for you – it’s for them. To do that, you need life insurance that protects your partner or children as long as they’re financially dependent on you. For example, some new parents buy 20-year policies to cover their children until they’re out on their own. If you want an extra cushion to cover their college years, a longer policy might be better. Don’t forget older dependents, too, like senior parents or relatives.

Your Debts

The average American has more than $90,000 in debt, according to a 2021 Experian study. That includes all forms of debt, including mortgage debt, student loans, and credit cards. The payout from a life insurance policy can help cover those debts, allowing your family to stay in their home or manage mounting bills in a time of loss.

Whether you’ve just bought a new house or are halfway through a 20-year mortgage, that timeline can help you calculate how long you need coverage. Medical bills, credit card debt, and student loans can usually be paid off quicker, so if those are your only obligations, a shorter term may work best. If you have a mortgage, make sure your policy will last at least as long as your payments. Consider debts of all types, secured and unsecured, as well as debts you may have in the future. That may include costs associated with long-term care or medical bills.

Your Expected Financial Status

Another factor to think about is your financial status now and in the next few decades. If you’re nearing retirement and are buying a term policy for income replacement, you might not need coverage once you leave the workforce. Keep your ideal retirement date in mind and add a few years, just in case.

On the other hand, if you’re earlier in your career and just starting to build up your 401(k), you might need more coverage. Take a step back and consider the full picture. In the next 20 or 30 years, could your family still be very reliant on your paycheck to meet their needs? If so, a longer-term policy may fit your lifestyle better.

How Much You Can Afford

Shorter policies cost less when you buy them, but if you end up needing life insurance again, you may find yourself buying a similar policy at a higher rate as you get older. Try to look ahead and remember that even long-term policies tend to cost less when you’re young and healthy.

What are the different policy term lengths?

There are four main term life policy lengths, ranging from 10 to 30 years. They all offer different advantages, depending on your needs and financial situation. Let’s take a closer look at each one.

Who needs 10 year term life insurance?

“How long should I get life insurance for if I’m older?” If you’re just a few years out from paying off your big financial obligations, a 10 year term life insurance policy can provide protection right when you need it.

A 10 year term life insurance policy provides a guaranteed death benefit and level premium throughout the life of the policy. As long as you maintain the premiums for the policy, it remains in place for a decade to help your beneficiaries if you die during that time. A 10 year policy can work well if you:

- Plan to retire in the next five to 10 years. Just have a few years left in the workforce? If you’re on track to retire comfortably and you’ve paid off the house, a 10 year term can keep you covered until you’re financially independent. If something happens during that time, your family has a cash cushion to replace those last few years of income.

- Have just a few years until your kids are grown or your mortgage is paid off. Again, a 10 year plan can offer short-term protection if you’re still wrapping up major financial responsibilities. Make sure to give yourself a little extra wiggle room on your term length – if you have 11 years left on your mortgage, consider rounding up to a 15-year policy.

- Are in your 50s or 60s. As you get older, some companies may no longer offer longer term lengths. A 10-year plan can still provide affordable protection in your older years.

- Expect to improve your health in the next decade. Improvements to your health can have a big impact on your rates. For example, smokers working on quitting might choose a 10-year policy to keep them covered until they’re eligible for tobacco-free rates.

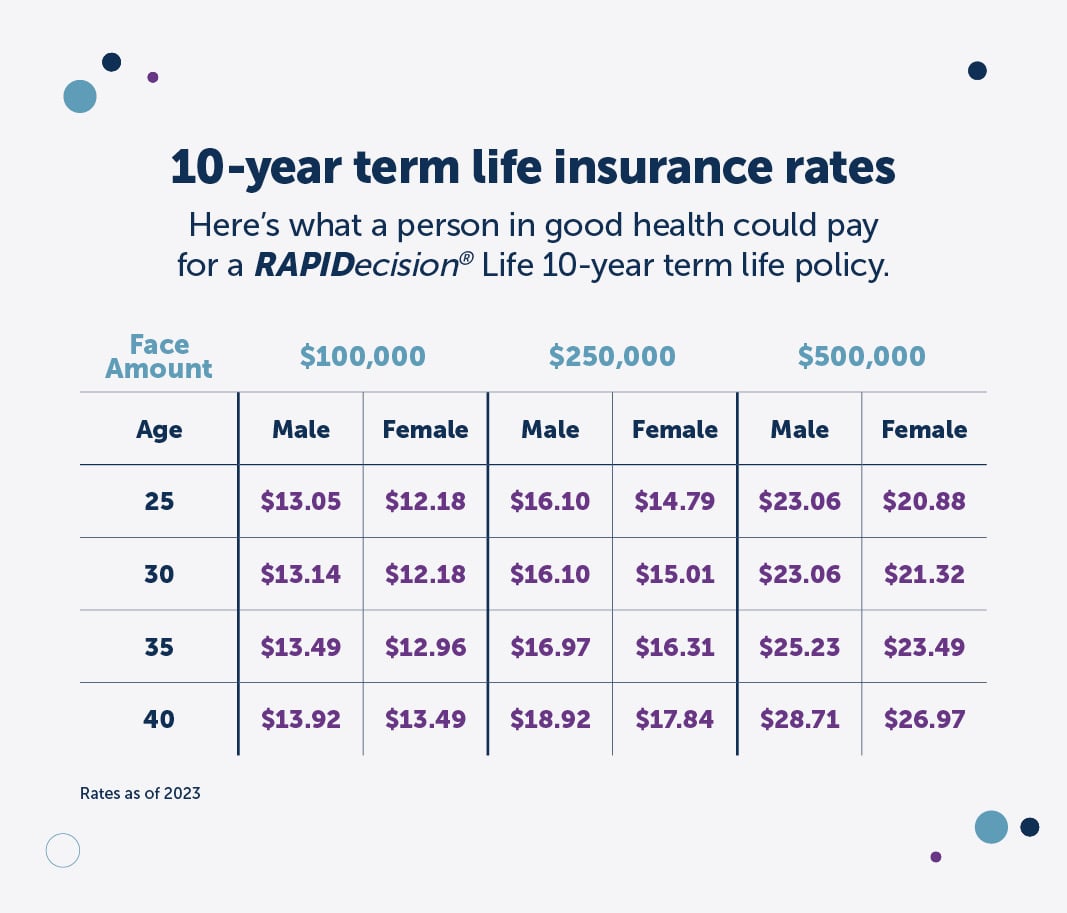

How much does a 10 year term life policy cost?

Here’s what a man or woman in good health might pay for a RAPIDecision® Life term plan from Fidelity Life. These are monthly premium payments for a non-nicotine policyholder.

Who needs 15 year term life insurance?

A 15 year term life insurance policy can be a solid investment for both older and younger buyers. A 15 year plan is generally more affordable than 20 year or 30 year policies, but keeps you covered longer than a 10 year policy.

You may benefit from this type of life insurance if you:

- Have kids in elementary school. If your children are already school-age, a 15 year term can replace your income until they’re safely out of the house. If anything happens to you in the meantime, they’ll have a way to cover daily expenses and put aside money for long-term goals, like college.

- Just took out a 15 year loan on your home. Many people match their term life insurance length to their mortgage term. If you opted for an accelerated 15 year schedule instead of a 30 year mortgage, a 15 year term life plan will provide coverage until you own your home free and clear.

- You need to bridge a coverage gap. Say you bought a 20 year term policy in your early 30s, but your mortgage is taking longer than expected to pay off or you added a child to your family later in life. Once your policy ends, a 15 year policy can tide you over until retirement at a lower cost than buying a 20 year or 30 year plan.

- You expect to be financially independent within the next 15 years. If you’re earning more than you ever have before in your career, those last few years before retirement are especially critical for your family’s long-term stability. A term life policy could cover your risks for the next 15 years.

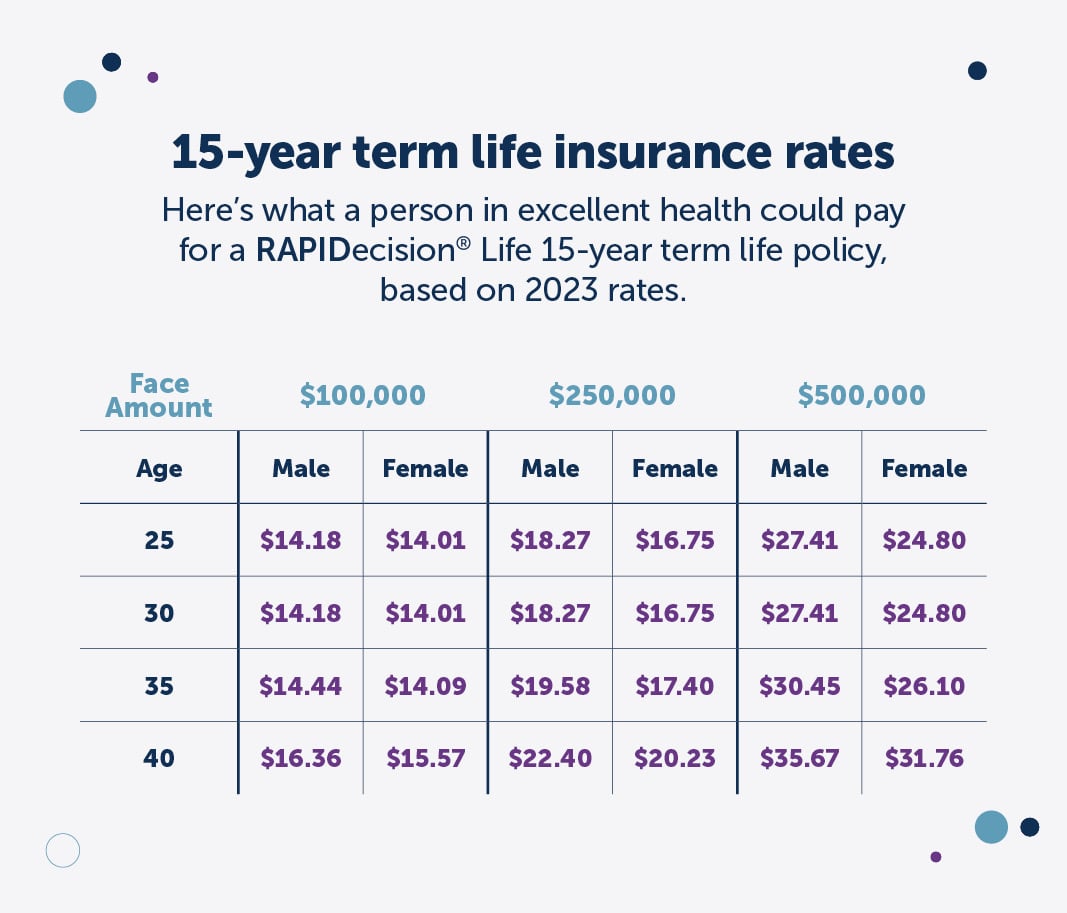

How much does a 15 year term life policy cost?

Here’s what a man or woman in good health could pay for a RAPIDecision® Life term plan from Fidelity Life, based on 2021 rates for a non-nicotine user. These are monthly premium charges.

Who needs 20 year term life insurance?

A 20 year plan is an affordable way to gain the peace of mind that you’re covered for the long term. A popular choice for many families, this type of coverage offers protection for decades at a lower cost than 30 year plans.

Looking forward, do the next 20 years of your life include dependents and financial obligations? If so, a 20 year term life insurance policy may be an ideal investment. Like other plans, you can count on the level premiums during this term. You may benefit from this length if you:

- Are early in your career. It’s a long road ahead, but you recognize the risk that the loss of your income could cause for your family. If you’re in your 30s or 40s, a 20 year policy can help them replace your paycheck until you’re close to retirement age.

- Have young children or a mortgage. Much like a 30 year term, many people choose a 20 year term to carry them through big life milestones like raising kids and paying off a home. If you’re not as concerned about having extra wiggle room at the end of your term life policy, a 20 year plan could meet your needs.

- Are budget-conscious. Term life is already more affordable than most people think. That said, a 20 year plan will offer savings over a 30 year one, especially if you’re in your 40s or older. Weigh the costs of coverage versus how long you think you’ll need protection to make the right choice for you and your family.

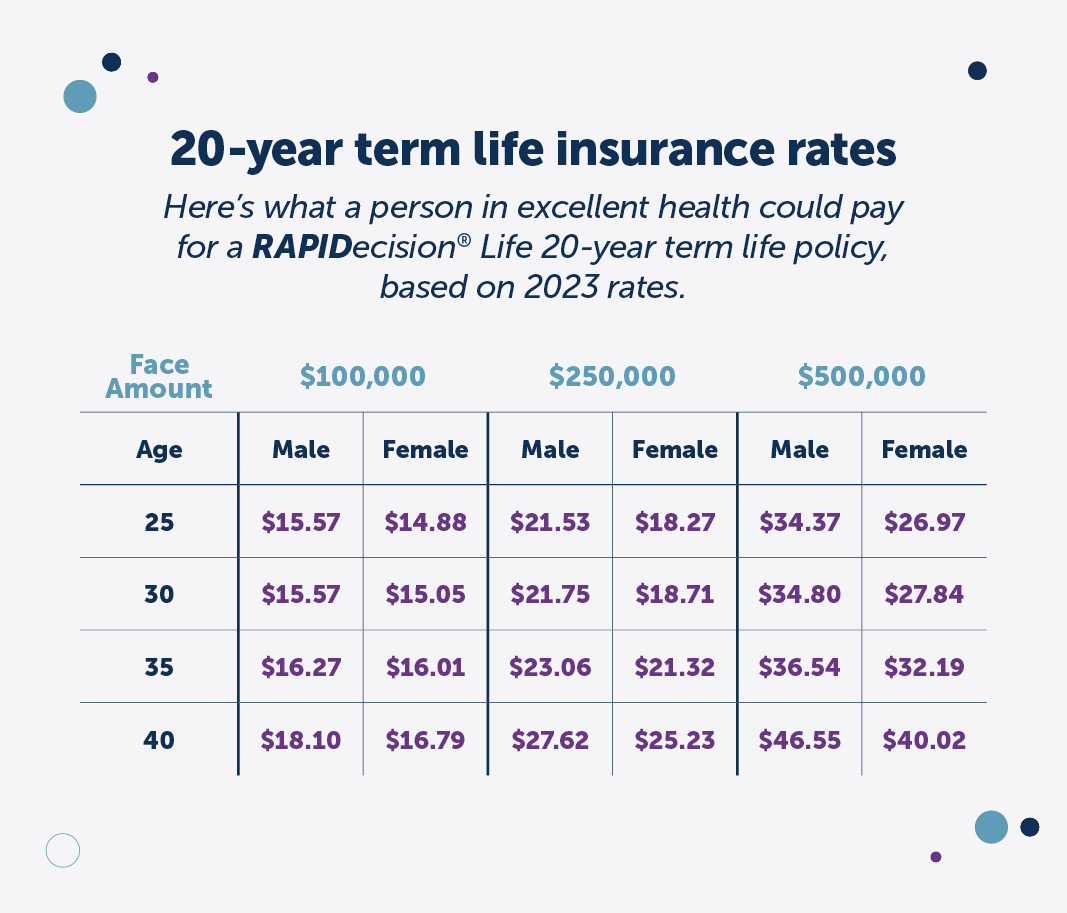

How much does a 20 year term life policy cost?

Here’s what a man or woman in excellent health could pay for a RAPIDecision® Life term plan from Fidelity Life, based on 2021 rates.

Who needs 30 year term life insurance?

This is generally the longest coverage available for term life, offering decades of flexible protection without the price tag of permanent insurance. A 30 year policy often makes sense for people who are just starting out in life, taking you from newlywed to empty nester or first-time homeowner to debt-free senior. Keep in mind that term life insurance isn’t always available to everyone at this length. If you have health concerns or you’re older, you’ll qualify for a shorter-term policy instead.

Wondering if a 30 year plan is right for you? A 30 year term life insurance policy can be a solid fit if you:

- Just got married. If you have a whole lifetime ahead of you, this type of life insurance can stick with you through all of life’s ups and downs. A 30 year plan provides coverage as you and your partner build a life together, providing protection as you have kids, buy a home, and advance your careers.

- Are ready to buy a home. What does life insurance term length mean to you? For many people, it’s about covering their biggest and most important investments, like a home, so that their family has a place to live no matter what happens. If you’re securing a mortgage now, it may be the ideal time to lock in a 30 year policy.

- Are a new parent. A 30 year policy can last from the years your little one is in diapers to the time they’re having babies of their own. If you’re a new parent or planning to have several children, a 30 year plan provides ample protection for families for decades.

- Are just starting out. Even if you’re still single and renting, it can be smart to lock in coverage now while you’re young and healthy. The younger you are, the lower your costs will be. With term life insurance, your rates will stay the same through the entire policy, even if your health changes.

- You have dependents with special needs. If you have dependents who will need financial protection even into their adult years, you may benefit from a 30 year term policy. It provides a longer-term safety net to provide financial support if something happens to you, but is more affordable than purchasing a permanent policy.

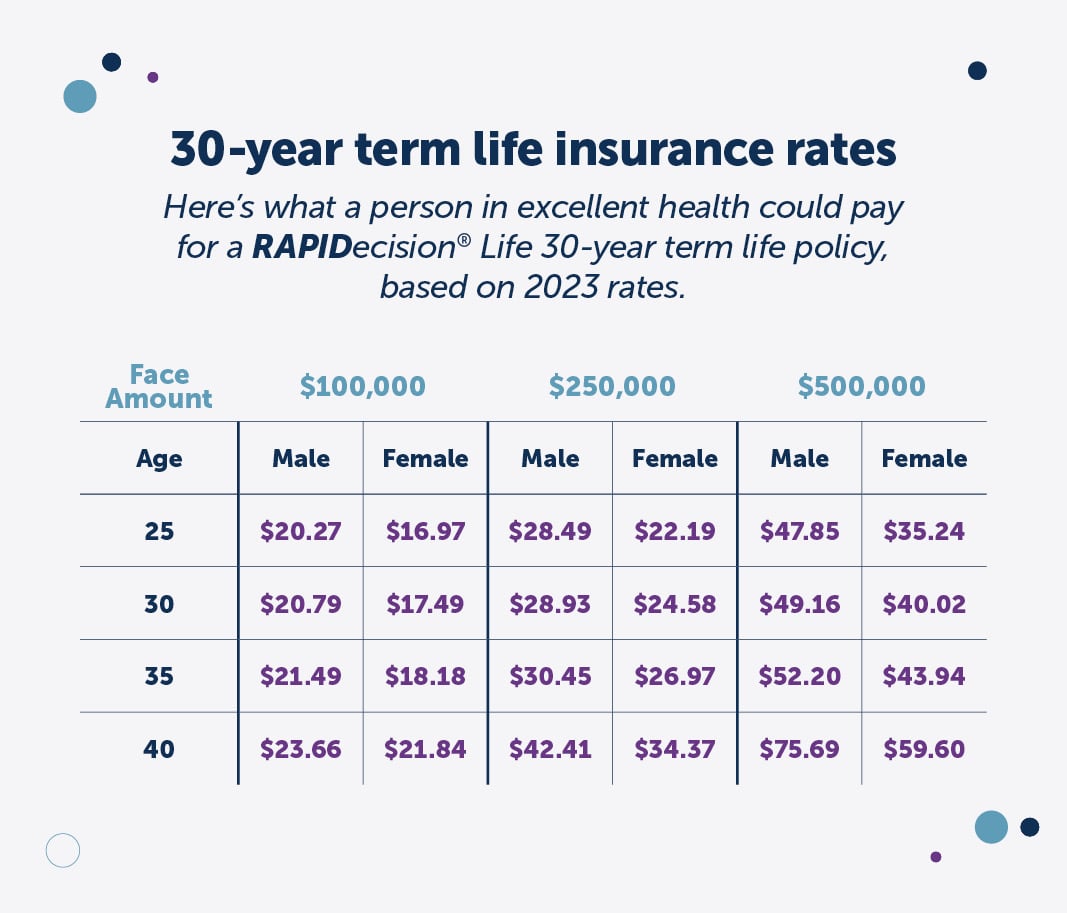

How much does a 30 year term life policy cost?

Here’s what a man or woman in good health could pay for a RAPIDecision® Life term plan from Fidelity Life. These are monthly premiums for a non-nicotine user.

Choosing between 20 vs. 30 year term life insurance

When it comes to 20 vs 30 year term life insurance, it can be tough to know what’s best. Both might seem like a long time when you’re in the prime of life. Choosing a shorter term length can mean shaving a few dollars off your payments, but going too short may cost you later.

If you reach the end of your term and find you still need coverage, your options are typically to renew your existing policy or buy a new one. In both cases, you’ll pay significantly higher rates based on your age. If you buy a new policy, you’ll also need to reapply – which could be difficult if you’ve developed health issues or other risk factors since you last bought coverage. A longer-term plan may cost more now, but that extra cushion can be worth it at the end.

Before choosing between 20 or 30 year term life insurance, think about the advantages of each based on your own financial situation, budget and goals. Here’s a breakdown of the pros and cons for each type of policy.

Pros of a 20 year term life insurance policy include:

- It’s less expensive than a 30 year policy. If you feel confident your financial obligations will be wrapped up in the next two decades, you can put that difference in premiums into savings instead.

- It’s available to more people. If you don’t qualify for a 30 year policy, a 20 year plan can still offer the long-term protection you need.

Cons of a 20 year term life insurance policy include:

- You’re buying less protection. There’s no way around it – you’re shaving off 10 years of protection from your life insurance by going with the shorter term. If your plans change, you could find that your financial safety net runs out while you still need it.

- You could end up paying more in the long run. If you find yourself in the situation above, you’ll likely need to buy coverage at a higher rate. That could end up erasing the savings of originally buying a shorter policy.

Pros of a 30 year term life insurance policy include:

- It’s long enough to cover most financial obligations, including mortgages. Three decades of life insurance can provide enough protection to carry you through a big chunk of your lifetime, even as things change.

- You can lock in affordable rates for longer. Since your rates stay level for the full length of the policy, buying a 30 year plan while you’re young and healthy can help you get a deal on a longer-term plan. The longer term length can also help you avoid the surprise cost of needing to buy extra coverage to bridge an unexpected gap later in life.

Cons of a 30 year term life insurance policy include:

- It costs more than a 20 year plan. This is a primary reason people opt for shorter term lengths. Per dollar of coverage, a 30 year plan will cost you more in premiums than a 20 year policy. If you truly don’t need the extra protection – like if you’re halfway through your mortgage and the kids are well on their way to adulthood – it can be better financially to buy the 20 year term and save the difference.

So which is the better option for you? That decision is up to you and your family. Ultimately, the right choice comes down to how much you can afford, how risk averse you are, and how likely it is that your financial situation will change in the decades to come. Our team at Fidelity Life can help you compare your options so you can shop and buy with confidence.

Have more questions about term life insurance?

We’re here to help. Get in touch with us to talk to an agent or start your online quote today.

At Fidelity Life, our goal is to make life insurance simple, affordable, and understandable for everyday families. This content is intended for educational purposes only. Each post is carefully fact-checked, reviewed, and updated regularly to ensure the information is as relevant as possible.