From the first moment you cradle your baby in your arms, your priorities start to look different. As a new parent, you want to give your little one everything they need to flourish in life. That means many things will change, including your finances.

Take a moment to think about the coming years. Do you feel comfortable with the financial health of your growing family? If you have a child on the way or plan to have children in the coming years, how ready are you to meet all of their needs? Most often, parents need to do some financial planning to ensure a bright future for their children.

Do you have a financial plan? According to a 2020 study, over half of American parents haven’t saved for their children yet. The study noted that:

- 32% of parents have a regular savings account set up

- 13% have a 529 college advantage account to use for college investing

- 8% have money set aside in certificates of deposit or savings bonds

- 7% have money in a retirement account meant for their child’s needs

Saving for kids isn’t something to put off, especially when you consider just how much there is to plan for in the average household. Whether you’re an expecting parent, a new parent, or a parent that hasn’t taken the steps just yet to create financial stability, saving now is essential. A traditional savings account is just one component of a much larger financial puzzle to protect your child’s future.

What is the average cost of raising a child?

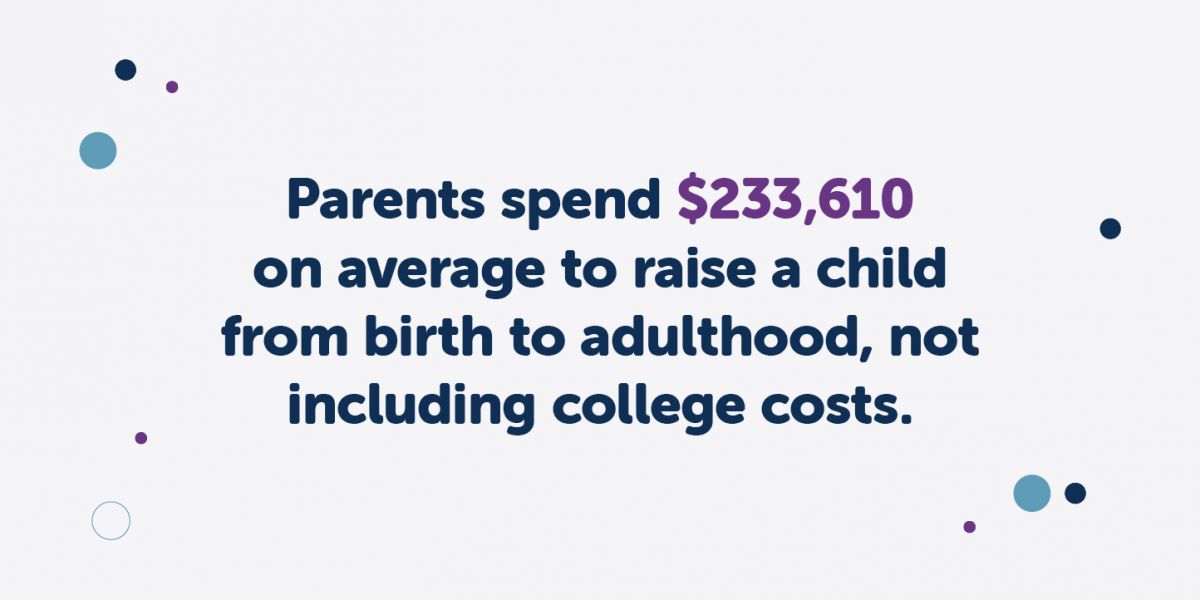

Parents spend $233,610 on average to raise a child from birth to adulthood, not including college costs, according to a 2017 U.S. Department of Agriculture study (the most recent research available). The organization predicted this figure would rise 2.2 percent per year based solely on inflationary costs, putting the total estimated cost above $250,000 today.

Some costs to think about include:

- The cost of labor and delivery: Parents can expect to pay anywhere between $5,000 and $14,500 for labor and delivery, depending on where they live, the type of birth, and the availability of health insurance.

- Typical baby costs: You’ll need to provide for all of their baby’s needs, like diapers, food, and cute onesies so they look their best. There’s also the need for cribs, diaper changing tables, and a car seat for each vehicle you own – which all adds up quickly.

- Day-to-day expenses: A bigger home may cost more in mortgage payments and utilities. You’ll spend more on food as your child gets older as well. Kids grow, meaning they need clothing, toys, school supplies, and much more with each year. Over time, you’ll need more of everything, maybe even a car if you’re relying on them to help with household responsibilities or driving a younger sibling.

- Childcare costs: Childcare costs are highly dependent on location, as well as how often you need to use their services. Childcare may range from $4,000 up to $22,600 per year for families based on age and location, according to the Economic Policy Institute. Check out the site for your state’s estimate.

- College costs: Whether your child goes to a community college or a private university, that’s going to cost money, too. For a private institution, the current annual cost is $35,087. For a public, out-of-state school, expect it to cost $21,184. For a public, in-state education, expect to pay $9,687. Don’t forget to factor in the growing cost of tuition.

Along with these expenses, consider the changing nature of your household’s finances. Many couples opt to have a parent at home, with more dads now joining moms in the stay-at-home ranks. The pandemic has also created big financial uncertainties for many families, with higher unemployment and furloughs reinforcing how important it is to have a nest egg in place.

Take a deep breath. Budgeting for a child can feel overwhelming, but you do have time to cover those costs (and taking a few steps today can help to make it easier). Being realistic about your situation now and both your short- and long-term goals can help you make better financial decisions for your child.

As you think about saving for your children, it’s important to plan for yourself as well. Parents often worry about their kids without thinking about their own financial well-being. Yet, if you don’t take steps to protect your own financial stability, no one else will do it for you.

So how do you do that? These tips can help you plan for your children properly and ensure your own financial security.

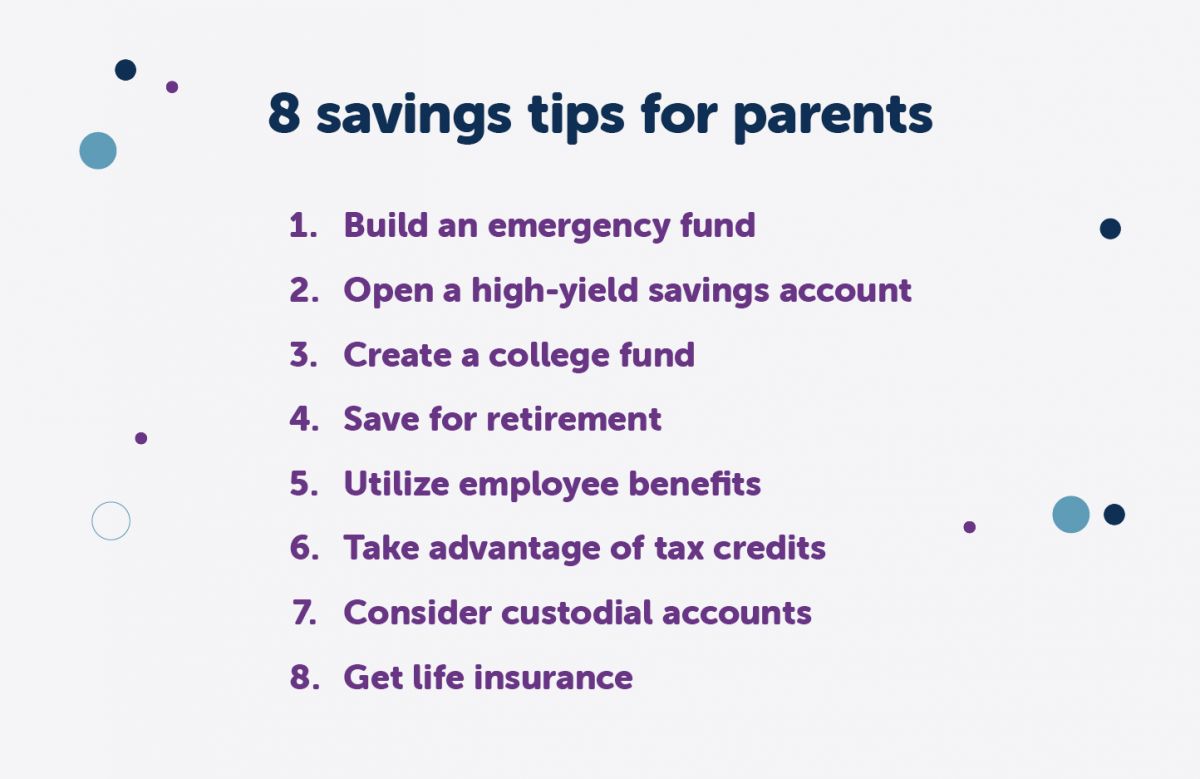

Build an emergency fund

An emergency fund is a simple savings account funded to include at least three months’ worth of expenses for your family. It’s even better to have six to nine months’ worth of essential living expenses tucked aside. In the case of a job loss, death, or other financial emergency, these funds can help cover immediate costs like the mortgage, health insurance, and food.

Even if you can’t reach that amount immediately, work toward establishing an emergency fund now. With as little as $1,000, you may be able to avoid turning to a credit card for unexpected expenses like car repairs or replacing a leaky dishwasher. Research shows that people who had an emergency fund in place during COVID-19 were half as likely to tap into their retirement savings to pay for their needs.

For families, creating an emergency account can seem hard to do, especially when you don’t have a lot of flexible spending money month-to-month. Here are a few tips to use:

- Set up automatic deposits into your savings account. Some banks allow you to set a specific dollar amount or a percentage of your paycheck to funnel directly into a savings account as soon as the funds hit your account.

- Create a budget that incorporates funding an emergency account. Stick with it, but make savings a core component of your monthly expenses instead of spending any extra money.

- Find ways to lower costs. That may include eating fewer meals out or carrying in, brewing your own coffee instead of buying it from the coffee shop, or carpooling to work or kids’ activities.

Each change you make to reduce your costs can help you build a stronger financial future.

While you’re working to build your savings, make sure to balance savings with paying down debts. If you’re earning 5% on a savings account and paying 20% in interest on credit card balances, you’re losing money. The key is to create a debt repayment plan to get those covered as soon as possible. Then, don’t use them to the point where you cannot pay them off in full each month.

Consider a high-yield savings account

What do you do with that emergency fund? You could open a basic savings account, but with interest rates low right now, it won’t do much for you in the long term aside from park your funds. A better option for many people is to open a high-yield savings account. This type of account has a higher interest rate than a standard savings account. Many of these accounts also skip the fees – as long as you maintain the balance within the account.

It’s not hard to find a high-yield savings account. Before you open an account, consider these tips:

- Know the minimum deposit amount. Most require a set amount to open the account.

- Find out what fees exist if your balance drops below the minimum requirement.

- Compare interest rates. There may be a significant difference from one bank to the next.

Using this option means you’ll tuck away money for an emergency and potentially earn from the interest applied to the balance. That can help you reach your financial goals a little faster.

Explore college fund options

That big price tag associated with college for your child (or children) can become more affordable if you start planning for it now, even if your child is still in diapers.

A 529 savings plan is a tax-advantaged option that allows you to pay for your child’s educational costs. (Newer models can also help cover the cost of K-12 education along with college.) These accounts allow you to choose between prepaid tuition or a savings plan.

A prepaid tuition plan allows you to pay for college costs now. This option is available in some states and with a handful of colleges. The benefit is you’re paying for tuition costs in today’s dollars, even though your child may not be ready for college for a decade or longer. The tuition plan grows in value over time. This plan covers just the cost of tuition, not other expenses. Once the time comes to pay for school, you don’t pay taxes on those funds.

A savings plan is more common. Here, you make contributions to the account over time. Most 529 plans are investments into mutual funds. You may have some flexibility in choosing your investment strategy. The value of the account grows based on how well the underlying investments perform. These funds can help a student pay for tuition, room, and board. There is no tax paid on these funds when you use them for educational expenses.

Start saving for retirement

Your next target for building financial security for yourself and your family is to think about retirement. 46% of Generation Xers don’t have confidence in their retirement savings.1 That number rises to 66% for millennials.2 Where do you stand?

The key reason to start a retirement account early is because you’ll need to invest less overall to reach your retirement goals, thanks to the value of compound interest. The longer your interest has to grow, the more value the account accumulates. Starting now, no matter your age, will make building a retirement easier than waiting even a few years.

Seek out a tax-advantaged plan to make your money work as hard for you as it can. This may include an employer-sponsored 401(k), Roth IRA, or a standard IRA. Compare options, such as deciding between a Roth IRA or employer-sponsored plan, to determine which one provides the best path toward building your retirement funds.

Utilize your employee benefits

Many employees have access to a few extras that can help them to maximize their paycheck. That includes a healthcare flexible spending account (FSA) or health savings account (HSA). These accounts allow you to put pre-tax dollars aside to pay for medical bills, prescriptions, or even personal care essentials like toothpaste and contact lenses.

Opening an account can help to make it easier to pay out-of-pocket costs your insurance plan doesn’t cover. It can also help you save more for retirement or for your children’s needs. The more money you don’t have to pay toward healthcare costs, the more you can place into your savings.

Take advantage of tax credits

As you look for the best way to save money for kids, think about tax credits. Working with an accountant can help you take advantage of all available tax breaks. However, there are a few simple things you can do now and on an ongoing basis to get the most out of these tax deductions and credits.

- The stimulus funds you’ve received (or may receive in the future) make a good way to boost your emergency savings account. If your emergency savings are in good shape, use them to pay down expensive debt or place the funds into your retirement account.

- Do the same for your tax return each year. Use these funds to tackle financial goals, reducing your need to pay interest over the long term.

- Take advantage of all tax credits. For children, that includes the childcare tax credit. You may be able to reduce what you pay the government in taxes each year by using available deductions (be careful, as they change rapidly).

- Set up a dependent FSA account. This can help you cover the costs of healthcare for your child and provide a tax break for you at tax time.

- Claim your mortgage interest. Your property taxes may be a tax deduction, too. All of this helps reduce your overall costs.

Working with a tax professional to ensure you file your taxes properly can help you avoid missing valuable deductions, too.

Consider custodial accounts

Along with saving plans for your child’s college costs, consider the benefits of a custodial account as well. These accounts, which are essentially a savings fund for your child’s use, can be a valuable tool for growing assets over time.

Most often, these college savings accounts allow you to establish the account in your child’s name, but they don’t have full access to the funds you set aside until they are an adult. Custodial accounts don’t offer the same type of benefits as a 529 college fund, but they do allow you to create another vehicle for building your child’s financial future.

Get life insurance

Finally, don’t skip life insurance. Beyond any other personal finance strategy, this is one of the most important and affordable financial tools to protect your child’s financial well-being. Should something happen to you, these funds can help provide critical financial support for your child. A life insurance payout comes with no strings attached to help pay for day-to-day living expenses as well as big investments, like college.

For most families, term life insurance is the way to go. These plans offer coverage for anywhere from 10 to 30 years, with coverage starting around $15 per month. You can match your policy length to the age of your child to provide coverage until they’re out on their own.

Permanent life insurance is more expensive, but can provide lifelong coverage if you have a child with disabilities or other ongoing financial responsibilities. These policies stay active as long as you keep paying the premiums, and also build cash value you can borrow from during the life of the policy.

At Fidelity Life, we offer a variety of life insurance options to cover a range of family situations. Our agents can help you review your options to cover your biggest investment: your children.

Still have questions?

We’re here to help. Get your quote online today or call one of our agents at (855) 291-6365.

At Fidelity Life, our goal is to make life insurance simple, affordable, and understandable for everyday families. This content is intended for educational purposes only. Each post is carefully fact-checked, reviewed, and updated regularly to ensure the information is as relevant as possible.

Article Sources:

- yahoo!finance. “Generation X confronts harsh new reality of retirement: unreadiness, https://finance.yahoo.com/news/generation-x-confronts-harsh-reality-130000625.html”

- CNN Money. “66% of Millennials have nothing saved for retirement, https://money.cnn.com/2018/03/07/retirement/millennial-retirement-savings/index.html”