Home » Life Insurance Basics » Permanent Life Insurance 101 » What is guaranteed issue life insurance?

Guaranteed issue insurance is a type of life insurance policy that is typically geared toward people with health conditions that prevent them from obtaining other forms of life insurance. Also known as guaranteed acceptance life insurance, guaranteed issue is typically a type of permanent life insurance.

With permanent insurance, your coverage lasts for your entire lifetime as long as you keep up with your premiums. If you’re older or have health issues, guaranteed issue whole life insurance can provide a guaranteed way for your family to pay funeral expenses, medical bills, or other expenses after your death.

When shopping for life insurance, keep in mind that this form of life insurance typically has a graded period of two to three years. If you buy a policy and then die while in that graded period, the policy may not pay out the full death benefit to your beneficiary. Rather, they may see a return on the premiums you’ve paid with some interest. Once the period is over, your loved ones are eligible for the full payout.

For people who are concerned about leaving behind medical expenses and other bills, guaranteed issue can help. While coverage amounts are lower and premiums are higher than other types of insurance, the no-questions-asked coverage that guaranteed issue provides can be a financial lifeline for your family. Here’s a closer look at how guaranteed issue policies work and how to determine if it’s right for you.

There are a range of affordable Fidelity Life products to choose from based on your situation and financial responsibilities.

When you apply for guaranteed issue life insurance, your insurance company will ask a few basic questions to approve you for the policy and set your rates. Most people who apply for a guaranteed issue policy typically cannot be turned down unless they fall below or above an age range requirement. Since there’s no medical exam, health questions, or review of your medical records, the application process is generally quick and simple.

You’ll also choose a coverage amount when you buy your policy. This death benefit is a “graded benefit,” which means it won’t kick in until after the grading period for your policy. During that graded period, your insurance company will simply refund your premiums with interest to your family if you die.

Once the graded period is over, your beneficiaries will qualify for the full payout amount. Your beneficiary is the person who receives your death benefit and can be a spouse, child, or anyone else you choose.

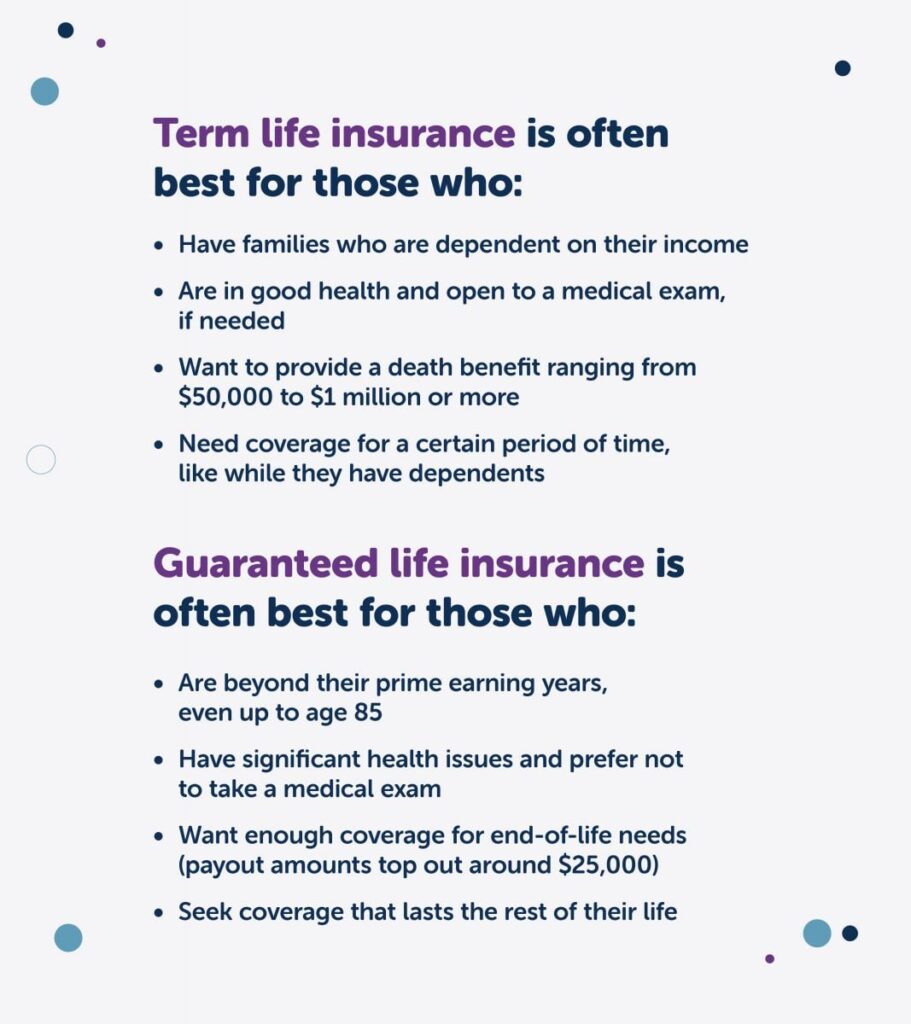

Some people may be disqualified from purchasing other forms of life insurance because of their age or medical conditions. If you’re in this situation, it can become much tougher to find financial peace of mind for yourself and your family.

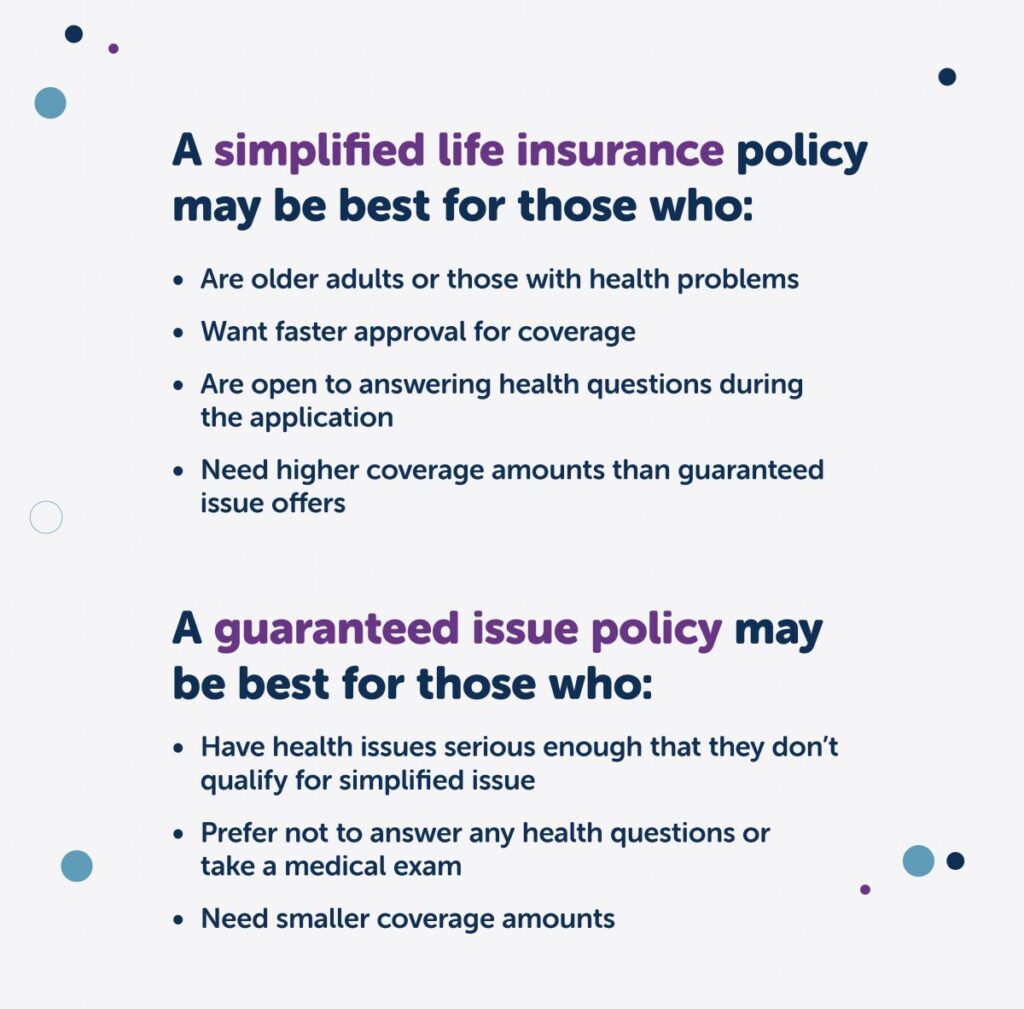

While you don’t need to be in perfect health to qualify for other types of policies, like term life or simplified issue life insurance, serious health issues often make you a better candidate for guaranteed issue. These conditions may include:

If you’re finding it difficult to obtain life insurance after a term life policy has matured, or simply because of health concerns or advanced age, a guaranteed issue policy can help you defray your final expenses, protect your family from increasing funeral and burial costs, or leave a small inheritance to a beneficiary of your choice.

It can also be beneficial to invest in a guaranteed issue life insurance policy when you take on sizable debt or want to leave behind funds for a specific charity. While the death benefit is not as high with this type of life insurance as with others, it can still help you accomplish financial goals after your death.

There are no real limits on how a beneficiary may use these funds in most cases. That means they can be helpful to cover specific needs unique to your family. Sometimes, the beneficiary may put those funds into a savings account as an emergency fund, too.

One other benefit? The death benefit typically is available quickly, helping to support short-term expenses for your family while they wait to settle your estate.

Many types of life insurance require a medical exam. Medical exams help your insurance company to assess your life expectancy to determine your eligibility and rates for certain types of coverage.

That’s where guaranteed issue life insurance is different. Since it’s intended for older people with potential health concerns, you can’t be turned down because of your medical history. There’s no medical exam to worry about or health requirements to answer. Depending on your insurance company, you may need to meet other requirements to qualify for a guaranteed issue plan, such as age limits.

Since insurance companies don’t consider your health when issuing your guaranteed issue policy, they price that into the plan. Rates are higher than other types of insurance for comparable coverage amounts, and the amount of coverage you can buy generally tops out around $25,000. With Fidelity Life’s RAPIDecision® Guaranteed Issue Life plan, you can buy up to $25,000 in coverage if you’re between 50 and 85 years old.

While coverage amounts are smaller than traditional term and permanent policies, that money can make a big difference for families to help pay funeral costs, nursing home bills, and more. Guaranteed issue whole life insurance is the ideal choice for many people who don’t qualify for a larger policy but want to leave behind money to a loved one.

Guaranteed issue whole life insurance is a type of permanent life insurance, which includes any policy that lasts your entire lifetime. When you’re shopping for coverage, though, keep in mind that guaranteed issue has a few key differences from other permanent plans.

Unlike guaranteed issue, permanent life generally requires applicants to be in good health. Many plans require a medical exam (although you can skip this step in most cases with Fidelity Life). If you’re older or have health complications, you may have limited choices for permanent coverage.

Similar to term life insurance, permanent life also offers larger death benefits. At Fidelity Life, you can buy up to $150,000 in coverage through our RAPIDecision® Senior Whole Life plans. That larger death benefit can help you leave behind more money to meet your financial goals, such as paying for a grandchild’s college education or making sure your spouse has enough to live on after you’re gone. If you’re in less-than-perfect health and just need enough coverage to pay for a funeral or other final costs, guaranteed life is often a good alternative to permanent coverage.

Finally, some permanent life plans have age limits or offer fewer choices for older adults. With Fidelity Life, though, you can buy RAPIDecision® Senior Whole Life coverage until you’re 85. This type of life insurance can help you fund bigger financial needs well into your older years.

Simplified issue and guaranteed issue life insurance share one big similarity: They don’t require a medical exam. You’ll still need to complete a full health questionnaire to qualify for simplified issue, including major illnesses or surgeries, family medical history, and any prescribed medications. However, there’s no actual medical exam involved. That typically means you can get approved faster than other types of policies, so it’s a good fit for people looking to get covered right away.

Overall, simplified issue has fewer health requirements than permanent or term life insurance, but more than guaranteed issue. If you don’t want to take a medical exam and don’t have major concerns in your medical history, this policy could be a good choice.

Simplified issue is also available in higher coverage amounts than guaranteed issue, although death benefits tend to be smaller than other types of term or permanent coverage. At Fidelity Life, our RAPIDecision® Final Expense simplified issue plans offer up to $35,000 in coverage to pay for funeral expenses, medical bills, or other final needs for your family.

Since it has fewer health requirements, simplified issue insurance is a little more expensive than medically underwritten plans, but more competitive price-wise than guaranteed issue. Some simplified issue policies are written as term policies, which means they remain in place for a set number of years. Others are written as permanent life coverage, remaining in place for the rest of your life as long as premiums are paid. This also affects how much you’ll pay for coverage.

The majority of guaranteed issue life insurance plans are permanent policies, which means they’ll last for the rest of your life as long as you keep up with your payments.

Generally, life insurance falls into two categories:

When you die, your family has a guaranteed payout to count on for whatever they need: paying funeral expenses, medical bills or nursing home expenses, covering mortgage or rent payments, or setting aside for the future.

If you know you want to leave behind a source of cash to ease financial burdens after you’re gone, guaranteed issue whole life insurance offers exactly that – a guaranteed way to do it. While the costs are higher and coverage amounts lower than other types of coverage, guaranteed issue can offer a path to financial protection when you don’t have a lot of other options. Being able to buy life insurance can bring you and your family much-needed peace of mind, especially if you’re aging or dealing with health issues.

While guaranteed issue term life policies are relatively rare, some group life term policies are offered on a no-questions-asked guaranteed issue basis. Group life typically includes any life insurance coverage issued through your employer, which may be free or low-cost to you. Companies often offer guaranteed issue plans to make approval easier for all employees, assuming that enough of their workers are healthy to offset the risks of insuring any workers who are older or have health issues.

Guaranteed issue coverage through your employer can be a nice perk, but group life policies tend to come with limitations:

If you’re considering a guaranteed issue term policy through work, think about supplementing it with your own individual term life policy. Shopping for guaranteed issue life insurance on your own? Your options will probably be permanent policies – which can help make sure you have coverage when it matters.

A guaranteed issue life policy from Fidelity Life can give you important financial protection with no medical exam or health qualifications.

Most guaranteed issue life insurance policies have relatively low death benefits, between $10,000 to $25,000. With Fidelity Life, you can qualify for a guaranteed issue policy with coverage amounts up. to$25,000 up to age 85.

Since guaranteed life insurance is a type of permanent policy, there is the potential to accrue cash value. It’s best to check with your insurer to understand how cash value accrues based on your policy.

Guaranteed issue is a type of final expense policy, but that doesn’t mean beneficiaries have to use the death benefit to cover funeral expenses. Your loved ones can use the death benefit to cover end-of-life costs, debt repayment, or any other way they see fit.

Most adults could benefit from having life insurance. Find out how life insurance can protect the life you’ve built and the people you love.

Get your life insurance quote online or call one of our agents at (866) 912-7775

Monday-Friday 8am to 5pm