Key takeaways

-

- A beneficiary is the person who receives the death benefit from a life insurance policy after the insured passes on.

- As a policyholder, you’ll need to name at least one beneficiary, and you can name multiple beneficiaries.

- Most beneficiaries are revocable beneficiaries, which means you can change who you name as the beneficiary later.

- An irrevocable beneficiary is a person who cannot be easily changed or removed from your life insurance policy.

Ready to get started?

What is a beneficiary?

Who do you want to protect financially when you die? The goal of life insurance is to provide a financial cushion for those people – called beneficiaries – after your death.

Beneficiaries are the people or entities that are entitled to receive a payout from your life insurance policy. When purchasing coverage, one of the key steps is to select beneficiaries.

Beneficiaries come in different forms: A primary beneficiary is the first person named in your life insurance policy. They are the first in line to receive benefits from your life insurance policy. A contingent beneficiary, or secondary beneficiary, is a second party listed on the life insurance policy. If your primary beneficiary dies before you, your secondary beneficiary will receive the benefits from the policy. You can name multiple primary and secondary beneficiaries.

It’s also important to know a beneficiary does not have to be a person. For example, you may name a favorite charity as your beneficiary to receive your life insurance payout.

Another designation to keep in mind is revocable or irrevocable beneficiary. A revocable beneficiary is a named beneficiary who you can change later if needed. While this is the most common type of beneficiary, some people choose irrevocable beneficiaries. Once you name an irrevocable beneficiary on your policy, you can’t change the beneficiary without their consent.

How do you know who to choose as a beneficiary? What type of beneficiary should you select – revocable beneficiary vs irrevocable beneficiary? There are a few things to keep in mind to make sure your payout goes where you intended.

What Is a Revocable Beneficiary?

Most life insurance policies have revocable beneficiaries. In this type of life insurance policy designation, the owner of the policy remains in control.

As a policyholder, you can change your revocable beneficiaries or change the percentage of the payout that goes to each beneficiary. Your beneficiaries don’t have a say in any changes you make, and changing your beneficiary is usually as simple as filling out a form. Going this route gives you the flexibility to change beneficiaries at any time during the policy as your situation and priorities change.

What Is an Irrevocable Beneficiary?

An irrevocable beneficiary has specific rights to your policy. For example, they:

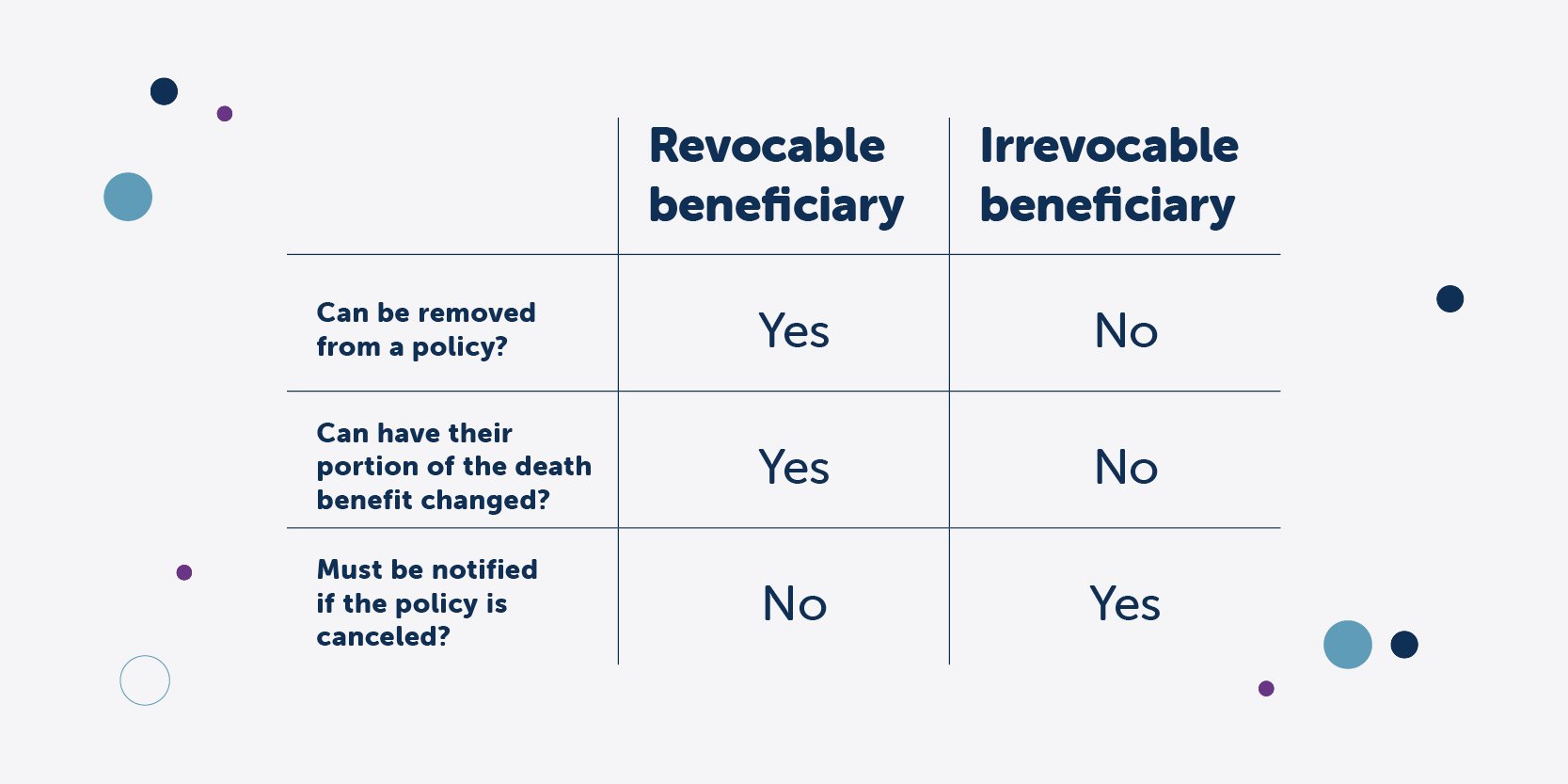

- Cannot be removed from the policy as a beneficiary without their consent.

- Cannot have their share of the death benefit changed without their consent.

- Have to be notified if the policy owner cancels the policy.

This impacts the policy owner in several ways. If you decide to change the beneficiary on your policy, you’ll need the current irrevocable beneficiary to sign off on these changes. That can be a much more involved process than updating a revocable beneficiary.

Some people may choose to name an irrevocable beneficiary if they want to guarantee that a certain person or entity will receive their payout. But as life speeds on, things often change. You may decide down the road that you want to change who receives these funds. That’s much more complicated with an irrevocable beneficiary designation.

Find a policy that works for you

There are a range of affordable Fidelity Life products to choose from based on your situation and financial responsibilities.

How do you designate an irrevocable beneficiary?

After you shop for life insurance quotes and select a policy, speak to your insurance agent about choosing an irrevocable beneficiary. First, make sure you understand what “irrevocable beneficiary” means for the specific type of insurance policy you’re purchasing.

Unless instructed differently, your life insurance company creates a revocable beneficiary designation when you purchase the policy. If you want to assign an irrevocable beneficiary, let your insurance company know. You may be able to update an existing life insurance policy to include an irrevocable beneficiary.

Why would someone name an irrevocable beneficiary?

As the policy owner, you can choose how you want to assign your beneficiaries, and you don’t have to tell anyone why you plan to do it that way. There are a few key reasons why you may go this route.

Key Man Policy

A key man policy is a life insurance policy taken out on a key member of a business. If the death of an executive or other leader could be potentially devastating to the business’ finances, this type of policy can help provide financial support to hire their replacement or make up for any lost business. Typically, the business owns the policy and is also the beneficiary. Since the company is paying the premiums, key man policies often list the company as an irrevocable beneficiary so that the death benefit is guaranteed to go to the organization.

Irrevocable Trust

Some families choose to create trusts to give themselves more control over how their assets are distributed later. You can add assets to a trust and create rules about how those assets can be used, like restricting them for a certain purpose or paying them out in installments over time. Much like an irrevocable beneficiary, an irrevocable trust is a trust that can’t be changed without the permission of the beneficiary. Naming an irrevocable trust as the irrevocable beneficiary of your life insurance policy guarantees that the trust will receive your payout when you die. This can help make sure the trust has funds available to cover your intended wishes, like paying for a child’s education.

Divorce Agreements

In some situations, you might name an irrevocable beneficiary due to an agreement in a divorce decree. If you and your spouse purchase life insurance during your marriage and pay into it, the divorce agreement considers this policy as an asset. In some states, that means the property accumulated during the marriage has to be split in an equal fashion.

In the case of a life insurance policy, that may mean listing the spouse as an irrevocable beneficiary. That means that they can’t be removed from the policy without their consent and will receive proceeds from the death benefit.

Ready to get started?

Is an irrevocable beneficiary the same as a primary beneficiary?

These two terms have different meanings when it comes to beneficiaries. The term primary (or secondary) refers to the order in which the death benefit is paid out at the time of the insured’s death. The irrevocable designation applies to the ability to change the terms of the policy.

In almost all cases, however, an irrevocable beneficiary is the primary beneficiary. That means they’re the first to be paid from the policy. Any other beneficiaries, if listed, will typically be secondary beneficiaries.

Assigning a beneficiary

When creating a life insurance policy, one of the questions your agent will ask is about your beneficiary. Choosing a revocable beneficiary is the most common option. It enables you to change the beneficiary or update the percentage of the policy a your life insurance beneficiary receives easily. That’s much more difficult with an irrevocable beneficiary, who needs to sign off and agree to this change.

At Fidelity Life, we know these are big decisions – and you want to make the right ones. Our team can answer questions for you to help you understand your options when assigning beneficiaries.