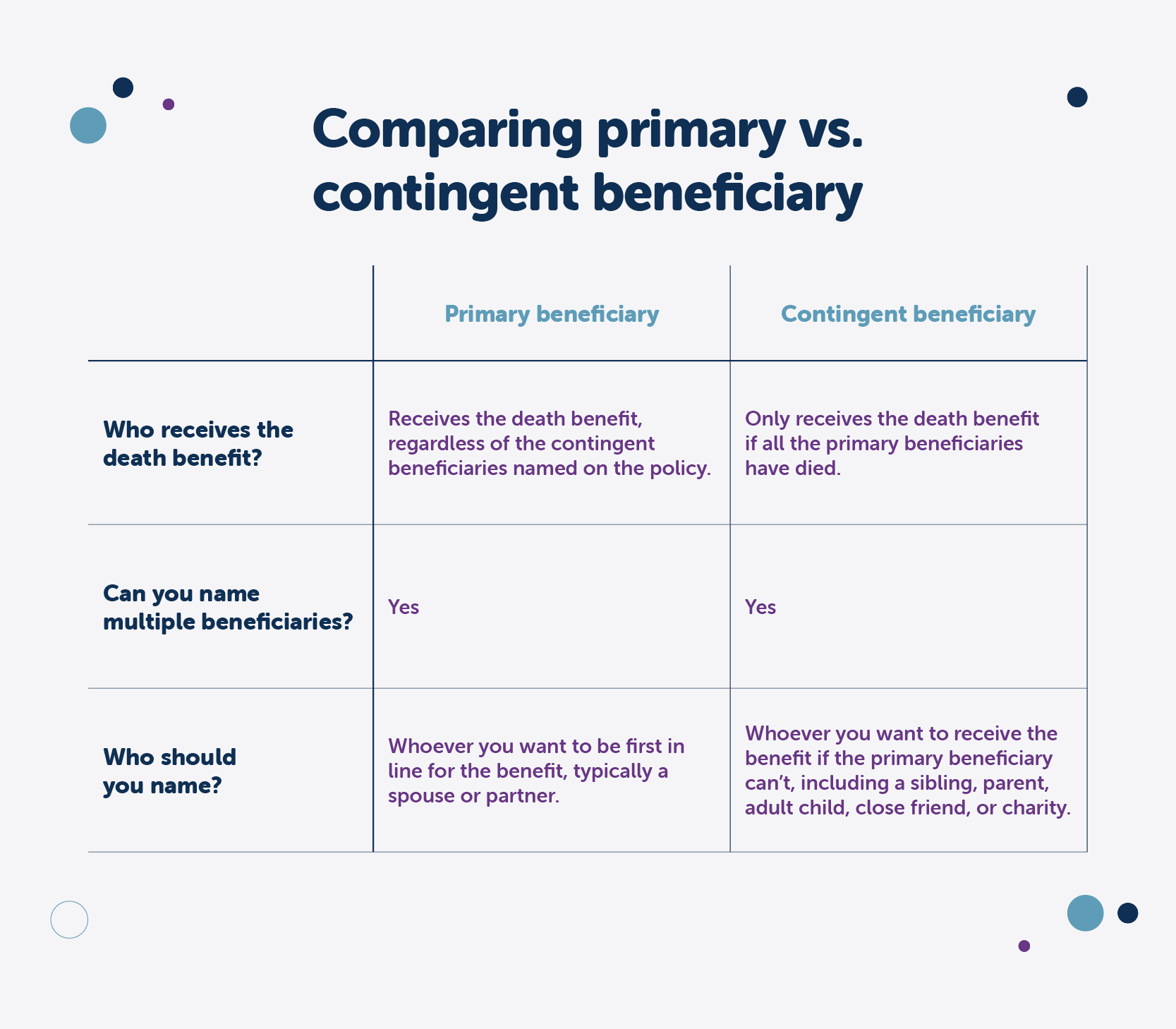

A contingent beneficiary receives your life insurance payout if your primary beneficiary has already died, is ineligible, or decides to not take the payout, helping make sure your policy supports your loved ones financially.

Life insurance is there to protect against the unexpected. But what if something unexpected happens to the person you planned to protect with your coverage? That’s why contingent beneficiaries exist.

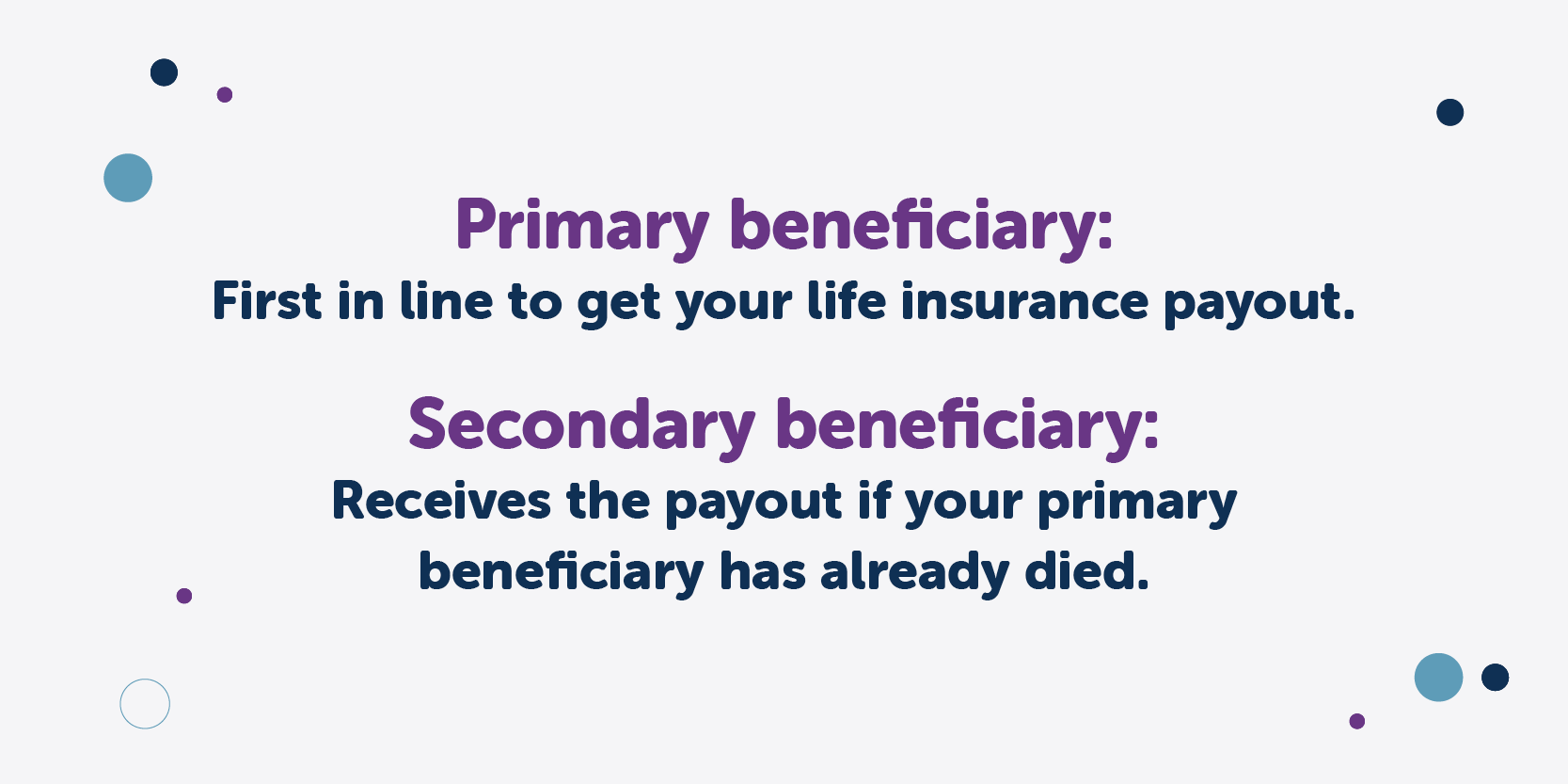

When you buy life insurance, you’ll name a primary beneficiary, like your spouse. This person is first in line to receive your payout, which they can spend on mortgage payments, daily bills, education costs, or anything else they choose.

It’s important to also name a contingent beneficiary, such as another close family member or friend. This person only collects the life insurance payout if your primary beneficiary is unable to collect it.

You can name more than one primary and contingent beneficiary, and you can also update your beneficiaries later on. Here’s how it works.

Do I need a contingent beneficiary?

Yes, you should name a contingent beneficiary in case anything happens to your primary beneficiary. If your primary beneficiary dies before you and you don’t have a backup, your life insurance payout will go to your estate and be subject to a legal process called probate.

It can take months for the court to distribute your money to your loved ones, which could leave them waiting for the financial support they need. If you have any outstanding debts, part or all of your payout may go toward paying them off. Naming a beneficiary allows your life insurance payout to sidestep the probate process, so your family can get the full amount they’re expecting shortly after your death.

To understand how contingent beneficiaries work, let’s say a woman gets on a plane with her spouse. Tragically, the plane goes down. The woman’s spouse is the primary beneficiary of her policy, but she’s also named her brother as the contingent beneficiary.

As the contingent beneficiary, the brother collects the death benefit payout without having to go through a lengthy court process. The brother can now use the payout for his sister and brother-in-law’s funeral costs, moving fees for their children to relocate to his home, and signing up their children for grief therapy sessions to deal with the loss of their parents – or anything else they may need growing up.

When do you need to set a contingent beneficiary?

Ideally, you should set up a contingent beneficiary when you buy your policy. That way, you have a backup plan in place right away.

If you want to add or change a contingent beneficiary later on, it’s easy to do. Most insurers will just ask you to fill out a simple form to update your beneficiaries.

Can I name multiple contingent beneficiaries?

Yes, you’re welcome to name more than one primary and contingent beneficiary. Keep in mind that your contingent beneficiaries will only receive a payout if all of your primary beneficiaries have died already.

If you decide to name multiple contingent beneficiaries, there are a couple of ways to split up your payout:

- The “per capita” approach splits your death benefit equally between all the beneficiaries. If one of them has died, the remaining beneficiaries split the payment. For example, if you named your three sisters and one passes away before you, your two surviving sisters would each get 50%.

- The “per stirpes” approach allows your death benefit to pass along to a beneficiary’s heirs, which can be helpful for large multigenerational families. Using the example above, if you named your three sisters as beneficiaries and one of them died before you, her children would each get an equal portion of her share of the benefit.

Who is the right person to be a contingent beneficiary?

Wondering who should be a contingent beneficiary on your policy? It’s important to name someone you trust to safeguard your family and their financial future. That could include:

Sibling(s)

If your spouse is your primary beneficiary, you may want to name your brother, sister, or spouse’s sibling as your contingent beneficiary. If you have children under 18, it’s smart to leave the payout with the same person you’ve named as their guardian if something happens to you.

Parent(s)

Similarly, if your parents or spouse’s parents are still independent, you can name them as contingent beneficiaries. They can use the money to provide for your young children or settle the mortgage on your home. If your parents are older and rely on you financially, you may name them as contingent beneficiaries so they can use the money to pay for their care and end-of-life costs.

Your adult children

While minor children can’t receive the payout directly from your life insurance, you may want to name your adult children as contingent beneficiaries. They can use the payout for anything, including paying off student loans, making a down payment on a house, or paying for a wedding. If something happened to both you and your spouse, this arrangement can give you peace of mind that your children’s financial needs are covered.

Close friend

Sometimes, friends become like family. In those cases, you may want to name a friend as a backup beneficiary to carry out your wishes. This arrangement often works well if you don’t have close family members.

Charity of your choice

A beneficiary doesn’t always have to be a person. If you have a cause that’s meaningful to you, you can name the charity of your choice as a contingent beneficiary. Since you’re able to name multiple beneficiaries, you can also split the payout between a charity and another friend or family member.

A custodian or trust

If you have young children but don’t have a relative or friend you can trust to care for them, you may want to set up a trust. Since your kids can’t receive your life insurance payout until they’re 18, you would name the trust as your contingent beneficiary to receive the funds. You’ll need to designate a custodian to manage the trust until your children are old enough to access it themselves. This can get tricky, so consult with an attorney about the specifics.

How to set up your contingent beneficiary

You can set up a primary and contingent beneficiary when you purchase a life insurance policy. If you already have a life insurance policy, you can often change your beneficiaries online at the Customer Account Center or contact your insurer to easily update or add a contingent beneficiary.

Still have questions about contingent beneficiaries?

We’re here to help. Get your quote online or call one of our agents at (866) 912-7775.

At Fidelity Life, our goal is to make life insurance simple, affordable, and understandable for everyday families. This content is intended for educational purposes only. Each post is carefully fact-checked, reviewed, and updated regularly to ensure the information is as relevant as possible.