What is life insurance underwriting?

Buying life insurance is a big step toward securing your family’s financial future. If you’re considering applying for a policy, you might be curious: What happens next?

When you apply for life insurance, whether that’s a term life policy or even a universal life policy, your life insurance company will review your application and other information to determine your eligibility and rates for your selected policy. This process is known as underwriting, and every life insurance company goes through some form of the underwriting process.

Wondering how long life insurance underwriting takes and what to expect along the way? At Fidelity Life, we’ve designed our underwriting process to make things easier and get you covered faster. Here’s how it all works.

How does life insurance underwriting work?

First, the basics of life insurance underwriting: Underwriting is a process your insurer goes through to confirm your eligibility and rates for a life insurance policy.

When you first apply for coverage, your life insurance company will let you know if you qualify for a policy and give you an approximate price based on the information you provide. After that, the company completes the underwriting process to make sure you’re approved for the plan and that the estimated price is accurate.

During underwriting, your life insurance company will review your completed application and the results of your medical exam, if you took one. In some cases, it may also verify information with third-party databases, like your prescription records. Companies use all that information to give you a life insurance classification, based on your overall level of risk to the insurer. The less likely you are to die while you own the policy, the better your classification will be.

Why do life insurance companies use underwriting?

The life insurance underwriting process helps your insurer to:

- Determine if you’re eligible for a life insurance policy

- Establish how much coverage you can buy

- Finalize the price you’ll pay for the life insurance

Wondering who’s making these decisions? Life insurance companies employ underwriters who are specifically trained to complete these tasks. In addition, many life insurance companies now use predictive analytics to help speed up the process. These technologies can help companies to verify information, source data, and determine rates and coverage based on company standards.

What makes underwriting life insurance with Fidelity Life different?

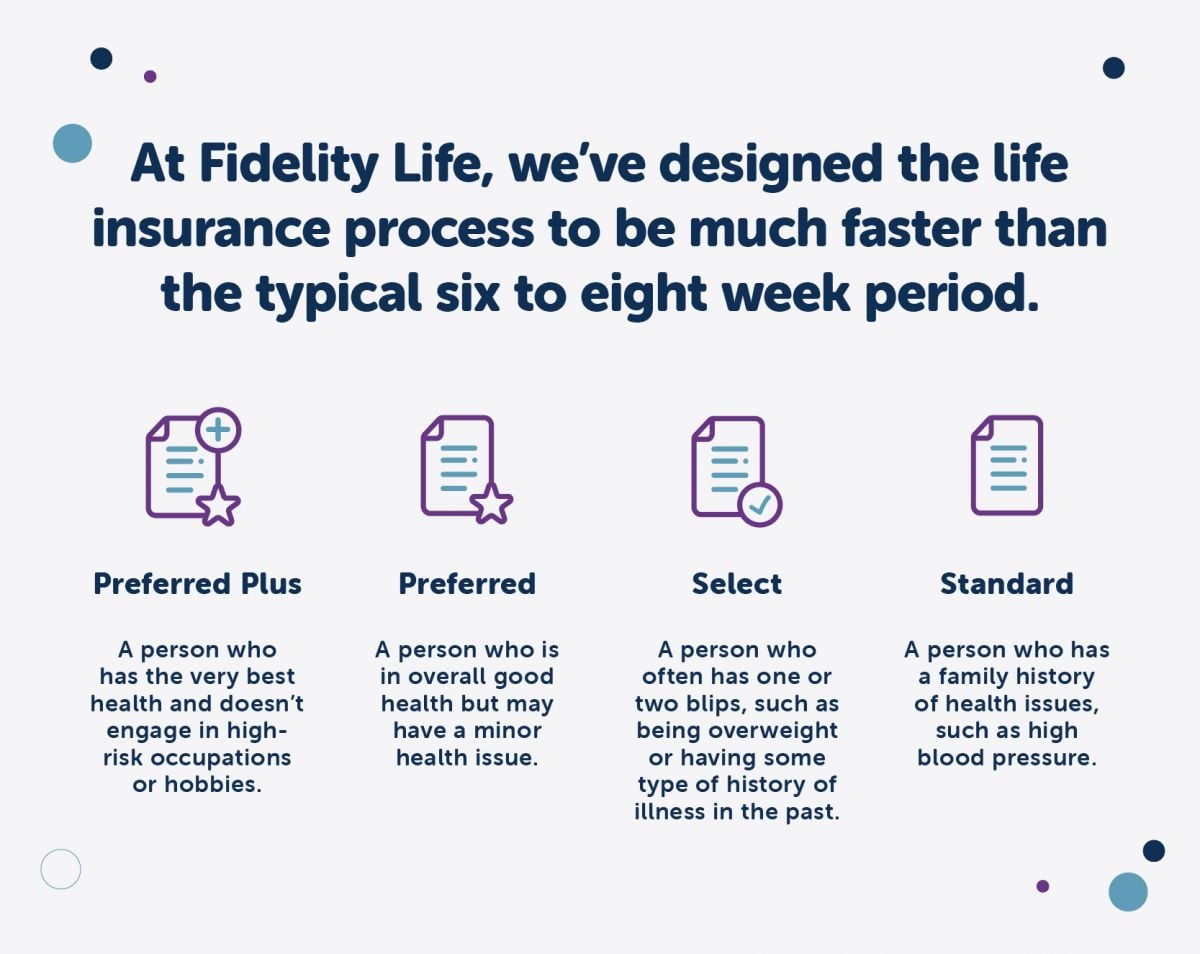

Sound like a lengthy process? Not anymore. While underwriting used to take up to eight weeks, technology is making the process much quicker. Fidelity Life was the first company to conclusively use predictive analytics at the point-of-sale to help some customers bypass their medical exams, and we’re continuing to find new ways to make the process fast and simple – including buying online.

Today, you can get approved for many Fidelity Life policies the same day you apply. That means your family has the protection they need, and you have peace of mind, sooner.

Which risk factors do underwriters consider for life insurance?

During the underwriting process for life insurance, your insurer will look at a handful of key risk factors. While each company’s process is a little different, there are a few common areas they’re likely to consider. Here’s the breakdown on what underwriters are looking for when they review your background.

Age

Your age is one of the biggest factors in qualifying for life insurance. Simply put, the younger you are, the lower the risk that you’ll die while the policy is active. That’s why, all other factors being equal, younger applicants get lower rates than older applicants. Life insurance policies also typically have age limits for coverage.

Even so, you don’t have to be in your 20s or 30s to buy life insurance. Many life insurance companies offer term life plans to people up to age 70, and final expense policies are available to people well into their 80s. And once you buy coverage, your premiums will stay the same for the entire length of the policy, even as you get older.

Gender

Your gender assigned at birth also has an impact on life insurance applications. Because women have a longer life expectancy than men, life insurance companies price that into their final premiums. That said, some states have adopted laws that prevent life insurance companies from offering different rates based on gender. Also, keep in mind that gender is just one component of the underwriting process. A 40-year-old woman with significant health issues is likely to end up paying more than a healthy 40-year-old man.

If you’re transgender, life insurance companies typically recommend that you list your assigned-at-birth gender on your application. This enables the insurer to underwrite the policy in a way that’s consistent with medical records. If a discrepancy is discovered between what is shared in the application and in medical records, this could lead to additional follow-up questions and a longer process.

Health

Along with your age, your health is one of the most significant life insurance underwriting factors. Your life insurance company will want to know your basic health information, including your height and weight, along with any major illnesses or surgeries. Other health-related factors include any chronic illnesses you have, prescribed medications, drug or alcohol use, and whether you smoke.

While being older generally means higher rates, it can also work in your favor with your medical history. For example, if you quit smoking 10 years ago, your life insurance company will give you a more favorable rating than if you just quit six months ago. With certain illnesses, such as cancers, insurers also want to see you’ve been in remission for at least a few years.

When you apply, provide as much detail as you can and be honest about any diagnoses or treatments. Even if you have a few concerns, it’s still worth it to apply for coverage. Many life insurance providers offer options for people who have had some medical issues.

Family medical history

Health history is a family affair for life insurance companies. During the application process, they’ll ask about your family medical history to learn if any close relatives have been diagnosed with conditions like cancer, diabetes, liver or heart disease, or drug or alcohol dependence. If anyone in your family has died suddenly before the age of 50, your insurer will want to know about that, too. These factors are all carefully considered during underwriting to determine how your family’s health might influence your own.

Occupation

Where you work can matter to insurers as well. Some jobs have an increased mortality rate that plays a role in what you can expect to pay for life insurance coverage. Working in an office, for example, is less risky than working on an oil rig in the middle of the ocean. Construction workers, military professionals, police officers, and lumber workers are a few examples of high-risk occupations. If your life insurance company determines you’re in a high-risk job, it can affect your eligibility and your rates for coverage.

Hobbies

What you do for fun can also play a part in which plans life insurance companies can offer to you. If you spend your weekends rock climbing the highest peaks or skydiving, those activities can increase your risk to insurers. Depending on how often you participate in extreme hobbies, it may influence your life insurance classification.

Your finances

Your income helps life insurance companies to understand how much your loved ones would struggle financially if you died. During underwriting, they’ll review your salary and other financial information to confirm you’re buying an appropriate amount of coverage.

It’s also important to be upfront with life insurance companies about your financial status, including any overdue bills or debt problems. If you’re looking to buy a large policy (typically $1 million or more in coverage), some life insurance companies may request your credit information via an inspection report during underwriting to verify you have a history of making payments on time. If that’s not the case, it could influence whether you qualify for coverage.

Driving record

Life insurance companies often verify your driving record during the underwriting process. That includes looking for any clues into risky behavior, like moving violations, driving under the influence, or other driving-related criminal charges. Underwriters base your classification on your record and how long it’s been since any driving-related charges were filed. A single speeding ticket a few years ago probably won’t matter, but multiple high-speed accidents will likely make it harder to buy life insurance.

Citizenship status

Some life insurance companies ask about your citizenship. Typically, companies offer life insurance coverage to U.S. citizens as well as permanent residents (green card holders). They may issue coverage for people who have a visa to live in the U.S. long term, but do not typically provide coverage to those with a work permit visa, student visa, or other short-term visas. If you’ve been in the U.S. for less than a year, you may find it harder to obtain life insurance.

Your address

Where you live plays a role in life insurance costs and availability, since not all life insurance companies operate in all states. During the underwriting process, they’ll consider which state you live in or are purchasing the policy in to determine which policies are available in your area and any state laws that apply to your coverage.

Coverage amount

How much life insurance do you want to buy? If you’re looking at a bigger policy, you may need to go through extra underwriting requirements, like additional health evaluations and a medical exam. Underwriters also compare the face amount of your policy with your financials to make sure the purchase is justified.

Any other policies or applications

Have you applied for other life insurance policies in the past? If so, make sure to indicate this on your current application. If you already have a life insurance policy in place and want to buy more coverage, provide that information, too. Insurance companies will look at the total coverage you own to make sure you’re not buying too much life insurance for your financial situation. Keep in mind this applies to individual coverage only, not any group policies through your employer.

Your beneficiary

On your life insurance application, you’ll need to provide information about your beneficiary. This is the person or people who will receive the death benefit if you die while the policy is active. You can name multiple beneficiaries, and you can also change them later if you need to. You can even name a charity as a beneficiary to support a cause that matters to you after your lifetime.

During underwriting, the life insurance company will check to make sure that you have an “insurable interest” in your beneficiary. Since life insurance is intended to support people who would suffer financially if you died, your insurer wants to confirm that’s the case. It’s easy to prove that your partner or other family members have an insurable interest, but you can’t name just anyone as your beneficiary. If you’re planning to make a non-family member a beneficiary, you’ll need to show some proof of a financial relationship with that person.

How does the life insurance underwriting process work?

Once you submit your application, the life insurance underwriting process begins. Each company has its own underwriting guidelines, so the process looks a little different from company to company.

Life insurance companies generally follow these steps to determine your life insurance classification and finalize your policy.

Review your initial application

Your application supplies a wealth of information that life insurance companies need to verify your eligibility and rates for coverage. During underwriting, they’ll look over your application carefully to confirm all the information you’ve provided is accurate and complete.

If small mistakes or errors crop up, the company will reach out to you to clarify any questions. This can hold up your application, though. Take the time to complete your application thoroughly and make sure everything is correct to potentially save yourself headaches later.

Also, be as honest and transparent as you can on the application. Since the insurance company will verify many of these details later through third-party sources, any incorrect data is likely to still come up. If your insurer finds out you withheld information intentionally, it could deny your application outright.

Evaluate your medical exam results

Some life insurance policies require a medical exam to determine how healthy you are. The exam is free of charge to you and similar to what you’d expect during an annual physical.

During the exam, a licensed medical technician will go over:

- Height and weight: Your height-to-weight ratio helps to indicate your BMI, which may be beneficial in determining overall health.

- Blood pressure: Taking your blood pressure can provide insight into your heart health. High blood pressure may indicate you’re less healthy or dealing with some type of underlying health complication.

- Health questions: These questions go a little deeper into your health history to cover areas like previous illnesses, injuries, and family history. Your insurance company looks at these answers, along with the information on your application, to get a full picture of your health.

- Blood tests: Having your blood drawn is a common part of the life insurance application process. It can provide insight into existing health conditions or areas of concern, including heart disease, diabetes, stroke risk, and the presence of blood-borne illnesses.

- Urine samples: in some situations, life insurance companies request urine samples. These can help insurers detect diseases or determine if a person is using drugs. Keep in mind that some insurers treat marijuana use with more leniency than others. You can always ask the insurer what their policies are before applying.

- Saliva samples: These samples are much like urine samples. They help to provide more insight into drug or tobacco use by the individual. This is done through a simple oral swab into your mouth.

During underwriting, the information collected from the medical exam is taken to a lab for analysis. Your insurance company uses those results to understand your health and confirm your eligibility and rates.

Don’t want to wait on a medical exam? With Fidelity Life’s RAPIDecision® Life plans, you can wait up to six months after buying coverage to take your exam. In some cases, you may even be able to skip it completely.

Check your attending physician’s statement (APS)

In some cases, the information from your application and medical exam might not be enough to complete the life insurance medical underwriting process. That’s where an attending physician’s statement (APS) comes in.

The APS is a summary from your doctor about your overall health. For those who have had health issues in the past, an APS can help your life insurance company clear up questions about your health. For example, if your medical exam showed you have high cholesterol, your doctor can explain any underlying issues and detail your treatment plan. This extra layer of information can help your insurer make more accurate underwriting decisions. If your application requires an APS, it may add a little extra time to the underwriting process, depending on how quickly your doctor responds.

Request additional reports

Underwriters often rely on additional reports from third-party agencies to shed more light on your application. These can include:

MIB records: This is a required check for most people. Medical Information Bureau records provide information about your previous applications for life insurance. If you’ve applied elsewhere in the last seven years, the information will be available here. During their review, insurers are looking to make sure none of your older applications contradict your current application. For example, if you disclosed previously that you smoked, but on the most recent application you stated you’ve never smoked, that’s a concern for the insurer.

Prescription medication records: Your insurance company may also source your prescription history. While they’re not concerned with the Z-Pak you took last year to treat strep throat, they’re looking for any medications you’re taking that may indicate more complex medication conditions. This lookback of your prescription history typically covers the last five to seven years.

Motor vehicle records: The life insurance underwriter also takes a look at driving records. Your previous driving records help to show if you’re a safe driver. Numerous instances of reckless driving tickets, for example, may indicate that that’s not the case. That means you are at a higher risk of being in an accident, including one that may cause your death.

Credit history: Some (but not all) insurance carriers look at credit history as well, especially if you’re applying for more than a million dollars in coverage. Your credit history can help indicate how financially responsible you are. Those who have a history of making late payments may find that this can impact their ability to qualify for life insurance or impact rates. They also look at any bankruptcies in your credit file or other data indicating you could be a higher risk for non-payment.

What are the life insurance underwriting risk classes?

After evaluating all the information from your application and other sources, underwriters give you an insurance classification. These classes indicate how risky you are for the company to insure and determine the price you’ll pay for coverage.

After evaluating all the information from your application and other sources, underwriters give you an insurance classification. These classes indicate how risky you are for the company to insure and determine the price you’ll pay for coverage.

As the underwriter works through the life insurance underwriting steps, they’re focused on risk. The more risk a person presents to the company, the higher their premium will be. Sometimes, too much risk means the insurance company may not offer a policy at all.

How does that all get determined? Every life insurance company has its own underwriting criteria and classification system. That means that the risk class one company assigns to you may be different from another. The main risk classes include:

Preferred Plus

This rating is sometimes called Preferred Best or Preferred Elite. It’s considered the highest rating possible. Those who fall into this classification are typically young and healthy, with no major or chronic illnesses, no high-risk occupations or hobbies, and no other big risk factors. As a result, people with this classification have the lowest life insurance rates.

Preferred

This policy is the next step down when it comes to risk level. This rating means a person is in good health overall, but may be older or have other minor issues that make them a slightly higher risk to the insurer. Preferred rates are generally affordable, and people in this rate class can choose from a range of life insurance options.

Select

The Select risk level is the next step down in terms of risk. If you receive this rating, there are a few concerns about your application. For example, someone with a Select rating might be overweight, have a chronic illness, or have a family history of illness. You’ll pay more in this risk class than someone with the Preferred rating, but you’re still generally a good candidate for coverage.

Standard

The Standard rating can be a bit confusing (isn’t average good, you might be thinking?) In life insurance, a Standard rating means your application raises some concerns for the life insurance provider. That could include significant health issues, like obesity or a family history of cancer. Life insurance may still be within reach, but you’ll pay more than someone with a Select rating and have fewer options overall.

There may also be more depth to these classifications. Some life insurance companies break down each of these rating classes further, with premium differences based on those sub-classifications.

In some cases, you may not meet the criteria for the rate classes listed above. This could be because of a significant health issue, high-risk job, or history of other risky behavior. Whatever the case, the life insurance company determines that you’re at a higher risk of dying at an early age.

When this happens, the insurer may approve you for a rated life insurance policy. This is sometimes called a substandard policy or a table-rated policy. This means you’ll pay higher rates than people in the main rate classes, but you still have some options available for coverage.

How long does life insurance underwriting take?

Traditionally, the life insurance underwriting process took anywhere up to eight weeks – or even longer if the insurance company needed outside resources, like a physician’s statement. At Fidelity Life, we’ve designed the life insurance process to be much faster, so you can have peace of mind much sooner.

We start your application on the spot as soon as you call, and we use information from public databases and other sources to help many customers get covered the same day. We offer a range of products that offer immediate coverage, including RAPIDecision® Life insurance. With RAPIDecision® Life, you can typically qualify right away for a combination of traditional life insurance and accidental death coverage, which provides a payout if you die in an accident. That means you’re covered while you complete a medical exam or any other requirements, so you can rest easy knowing that your family is protected.

Have more questions about the underwriting process?

We’re here to help. Start the life insurance process by getting a personalized quote or giving us a call.

At Fidelity Life, our goal is to make life insurance simple, affordable, and understandable for everyday families. This content is intended for educational purposes only. Each post is carefully fact-checked, reviewed, and updated regularly to ensure the information is as relevant as possible.