Life insurance isn’t a one-size-fits-all solution. As you get older and your family and financial situations change, there are different life insurance options to consider. For example, when you’re starting your career and raising a young family, an affordable term policy could be the best life insurance plan for you. However, if you’re an older adult looking to cover burial expenses, a final expense policy could be more suitable.

Regardless of which life insurance plans you’re considering, many people agree that there’s never a wrong time to buy life insurance. Still, those who have purchased a policy recommend getting insured sooner than later. In fact, according to LIMRA’s 2021 Life Insurance Barometer study, 39% of insureds wish they had purchased their policies at a younger age. So whether you’re looking for your first life insurance policy or debating how to protect loved ones as you approach retirement, we’ll break down the best life insurance plans at any age so you can find the right coverage as soon as possible.

Life insurance policy options

There are various types of life insurance policies, each with a unique set of benefits.

- Term life insurance provides coverage for your choice of 10, 15, 20, or 30 years. This type of insurance is usually the most affordable policy, as once the term ends, your coverage ends. With fixed premiums and death benefits, term coverage is an affordable option at any age.

- Permanent life insurance consists of whole and universal life insurance coverage. While each option offers lifetime coverage as long as premiums are paid, whole life has fixed premiums and death benefits. In contrast, universal life allows you to change premiums or death benefits if needed. In addition, permanent life insurance policies have a cash value component, making them more expensive than term life insurance. And while whole life offers a steady growth rate for your cash value account, universal life insurance cash value grows based on current interest rates.

- Group life insurance is coverage provided by work or another organization. These policies tend to be for smaller coverage amounts, meaning many group life insurance plans may not be enough to meet your needs. Therefore, it’s often wise to consider supplementing group life with an individual policy.

Best types of life insurance plans for different ages

No matter how old you are, there’s a life insurance plan to meet your needs and budget.

In your 20s

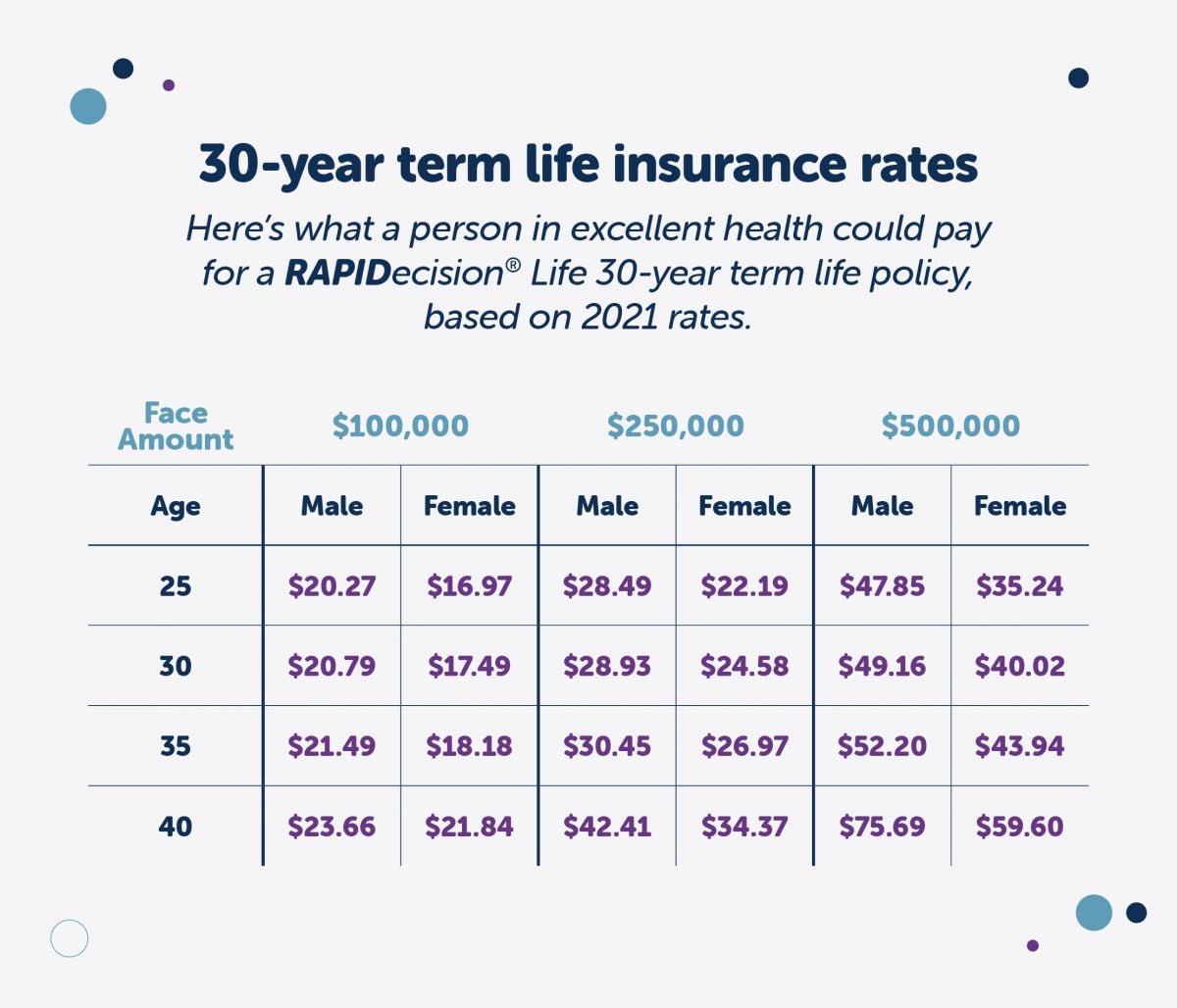

If you’re a young adult in your 20s, you may not have considered getting life insurance at all. But the reality is that getting a term life insurance policy in your 20s could be the most affordable option as rates are lowest when you’re young and healthy.

As you can see in the 30-year term rate chart below, securing life insurance at age 25 can generate significant savings compared to getting the same policy at age 35 or 40. And your savings increase as you get into larger coverage amounts.

A longer term policy, say 20 or 30 years, can give you peace of mind that life insurance will support loved ones across many stages of life, such as having a child and then seeing that child go off to college.

However, you may decide against locking in a life insurance policy if you’re debt-free and do not have any dependents. Even if that is the case, you can still use a policy to aid with final expenses or leave behind a gift for a cause or charity that you care deeply about.

In your 30s

Your 30s are a pivotal time when you may have more people depending on you, whether that’s a spouse or children. Plus, as you get older, whether to buy life insurance or how much to buy can shift from an independent decision to one you’re making with a partner. And regardless of whether each partner is earning a paycheck, you’ll likely want to consider getting a life insurance policy for both of you.

Term life is still likely the most affordable option in your 30s. However, whole life insurance might also be beneficial at this point in your life if you want to secure lifelong coverage at a reasonable rate. Permanent coverage is worth considering in certain situations, like if you have large financial obligations that aren’t time-sensitive or a dependent who may require lifelong financial support.

In your 40s

By the time you’re in your 40s, you may be married, have children, and even embark on a business venture or two. If you’re a business owner or business partner, you may have already taken out life insurance to secure a small business loan. But you’ll want to be sure your loved ones are covered too.

Purchasing a term life insurance policy in your 40s could provide 10, 20, or even 30 years of coverage as you face milestones like retiring, kids leaving the nest, and welcoming grandchildren.

You may also find your 40s are a good time to secure lifetime coverage if it makes the most sense for your family. Locking in a whole life insurance policy can give peace of mind that loved ones can cover financial obligations, no matter what the future holds.

In your 50s

Life insurance gets more expensive as you get older. However, there is still time to get an affordable term life insurance policy to cover you as the kids graduate school or you finally pay off the mortgage.

As you approach retirement age, your life insurance options will naturally focus more on your upcoming season of life. Fidelity Life’s RAPIDecision® Whole Life Insurance for Seniors can provide lifelong financial support for seniors who need between $10,000 and $150,000 in coverage.

If you’re feeling financially secure in your 50s, you may still want to plan for burial costs. After all, the average cost of a funeral is almost $8,000. Yet if your health status has changed over the years, you may not be comfortable taking a medical exam. That’s where a final expense life insurance policy comes in. Final expense coverage will only require a few health questions on the application. As a result, you can typically get coverage for up to $35,000, more than enough to help loved ones cover funeral costs and any other small outstanding debts.

In your 60s and older

During this stage of life, life insurance may support endeavors such as paying off a mortgage or supporting loved ones. Yet if you’re debt-free and no longer have dependents, you can still use life insurance to cover funeral costs and legacy planning.

Fidelity Life offers many life insurance plans for seniors, including:

- Senior Whole Life for those between 50 and 85 looking for a policy that builds cash value and never expires.

- Final Expense that can ensure end-of-life expenses, ranging from medical bills to funeral costs, are covered.

- Guaranteed Issue, which gets you coverage with fast approval and no medical exam or health questions.

Are you ever too old for life insurance?

You’re never too old to buy life insurance. Many life insurance providers, including Fidelity Life, insure up to age 65 and offer several policies for those up to 85. And if you have an existing term life insurance policy, you may be able to renew it into your 80s or later.

What’s a good age to get life insurance?

There is no right or wrong age to get life insurance. Life insurance is typically needed when someone relies on you financially, which can happen at any stage of life. So whether you’re in your 20s and want to cover paying the mortgage on your first home or in your 60s and want to make sure loved ones can pay for final expenses, there’s a life insurance policy to suit your needs.

Finding the right policy starts with getting a quote or talking to an agent by calling 855-544-9232.